Airlines rethink strategy as ecommerce to US begins decline

Shippers and forwarders are waiting to see how airlines manage their capacity before locking into ...

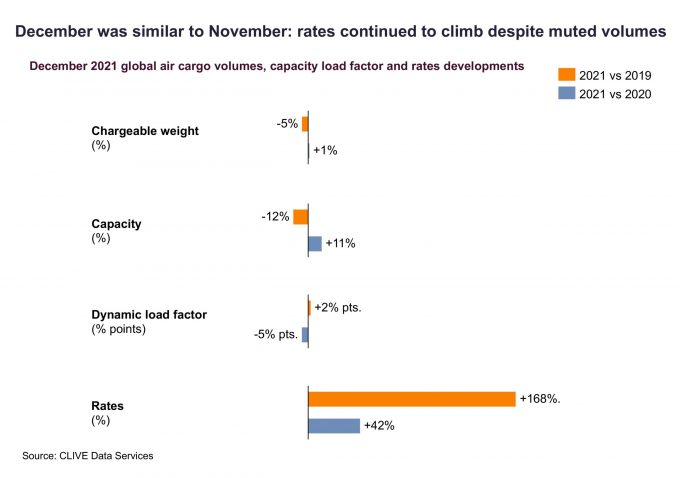

PRESS RELEASE

December demand in the general air cargo market put a final dampener on 2021 peak season volumes as continuing supply chain issues, congestion on the ground, and concerns over the new Omicron virus suppressed any end-of-year uptick, according to industry analysts, CLIVE Data Services.

CLIVE’s latest weekly market intelligence shows a -5% fall in chargeable weight in December 2021, compared to the pre-Covid level of December 2019, making it, versus 2019, one of the weaker months of the ...

Asia-USEC shippers to lose 42% capacity in a surge of blanked sailings

USTR fees will lead to 'complete destabilisation' of container shipping alliances

Outlook for container shipping 'more uncertain now than at the onset of Covid'

New USTR port fees threaten shipping and global supply chains, says Cosco

Transpac container service closures mount

DHL Express suspends non-de minimis B2C parcels to US consumers

Zim ordered to pay Samsung $3.7m for 'wrongful' D&D charges

Flexport lawsuit an 'undifferentiated mass of gibberish', claims Freightmate

Comment on this article