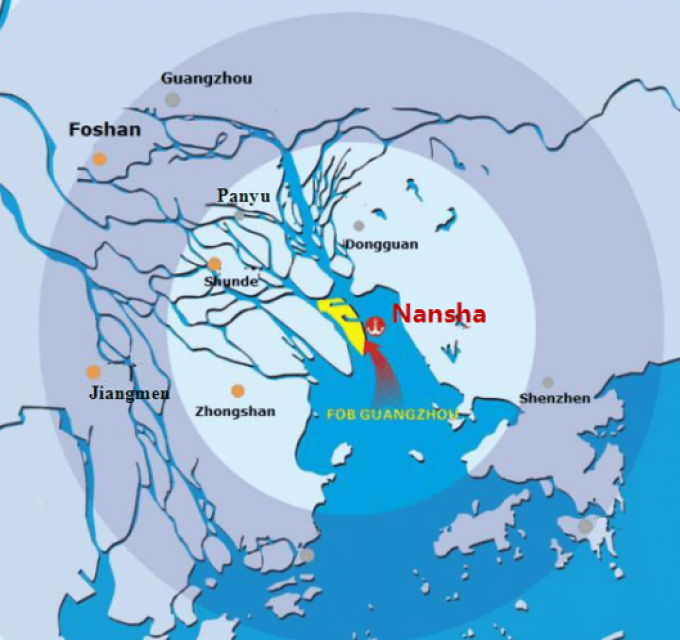

Container shortage worsens as box ships avoid Chinese ports that need empties

The availability of containers at southern Chinese ports continues to deteriorate as carriers omit calls ...

After the dust of 2020 has settled

Last year will go down in history as one of the most un-traditional years for a very long time.

While 2020 began as normal for the rest of the world, China announced in early January that it had been hit by a new coronavirus and that very strict measures were necessary to control its spread. For the rest of the world life continued as usual. This writer attended the Fruit Logistica Exhibition and Conference in ...

Asia-USEC shippers to lose 42% capacity in a surge of blanked sailings

USTR fees will lead to 'complete destabilisation' of container shipping alliances

New USTR port fees threaten shipping and global supply chains, says Cosco

Outlook for container shipping 'more uncertain now than at the onset of Covid'

Transpac container service closures mount

DHL Express suspends non-de minimis B2C parcels to US consumers

Zim ordered to pay Samsung $3.7m for 'wrongful' D&D charges

Flexport lawsuit an 'undifferentiated mass of gibberish', claims Freightmate

Comment on this article