Clear-up after toxic gas leak sees some Antwerp quays reopen

Antwerp’s Deurganckdok port area partially reopened today after an emergency services clean-up following Tuesday night’s ...

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

**EDITED AT 14:00 BST 02/04/25 TO INCLUDE QUOTE FROM ANTWERP-BRUGES**

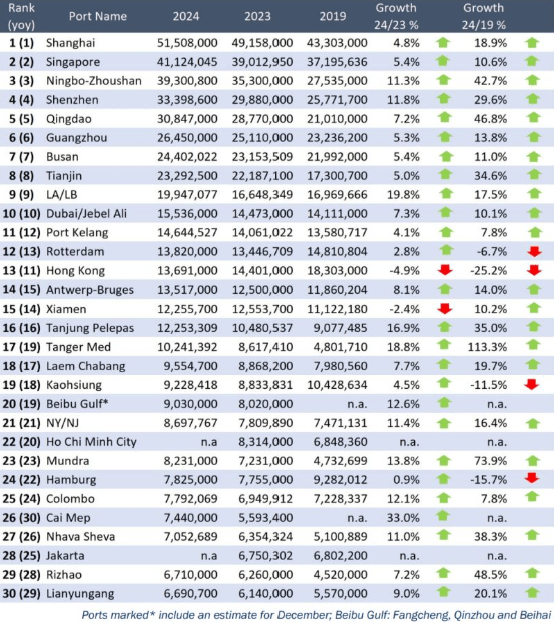

Last year’s port throughput “winners and losers” have been revealed, with Chinese ports still dominating across the board, and one European hub gaining market share above its neighbours.

Alphaliner data analysing port throughput across the world’s top 30 ports in 2024 found that “the big winners” of the year were Los Angeles/Long Beach, Tanger Med, Tanjung Pelepas and Mundra.

The biggest winner of those is arguably Tanjung Pelepas, which surpassed its own forecasted increase to 9m teu, reporting 10.2m teu total throughput for the year. Its volumes were up 113.3% from 2019, and its new role as the chief Asian hub for the Gemini Cooperation is likely to cement these volumes further.

Morocco’s Tanger Med rose from number 19 to number 17 in the list, posting an 18.8% growth to also reach 10.2m teu, a shade under Tanjung Pelepas.

“Tanger Med again enjoyed a stellar year, although some of the growth will be temporary, with the port benefiting from the Red Sea disruption… Not all of the gain can be attributed to the Houthi attacks, however, with the port citing around a quarter of the port’s volumes as Red Sea-related,” explained Alphaliner.

The Indian subcontinental ports of Mundra, Colombo and Nhava Sheva were also beneficiaries of the Red Sea crisis, reporting volume increases of 14%, 12% and 11% respectively from 2023.

Los Angeles-Long Beach’s success was attributed to strong US consumer growth as well as possible importer anxiety about the impact of tariffs, labour strikes and war-related disruption, added Alphaliner. The twin ports recorded 19.8% throughput growth in 2024 from the year before.

Meanwhile, only four ports in the top 30 had still failed to recover to pre-Covid levels – Rotterdam, Hamburg, Kaohsiung and Hong Kong – and only two ports registered a decline in volumes from 2023 – Hong Kong and Xiamen.

Hong Kong’s volumes decreased 4.9% from last year and are still 25.2% lower than before 2019, and is part of a long-term general decline in cargo traffic at what was the world’ largest container port two decades ago.

In Europe, Rotterdam and Hamburg recorded a throughput that was 6.7% and 15.7% below 2019, respectively, though both ports saw a modest increase in volumes from 2023 of 2.8% and 0.9% respectively.

A spokesperson for the Port of Hamburg told The Loadstar: “2024 was marked by numerous geopolitical and economic challenges… Specifically in Germany, economic output declined by 0.2% and industrial production also fell by 4.5% in 2024 compared to the previous year. Germany’s largest seaport was therefore faced with particularly huge challenges.

“Nevertheless, the Port of Hamburg has managed to return to growth in container throughput in 2024.”

However, Alphaliner data revealed that the nearby port of Antwerp-Bruges enjoyed a bumper year, recording an additional 8.1% throughput volume from 2023, and is now 14% up from pre-Covid levels – although Antwerp and Bruges were separate entities in the pre-Covid era, having formally merged in 2022.

Alphaliner’s Port of Antwerp-Bruges 2024 throughput data is compared to 2019 Port of Antwerp throughput data only. The port informed The Loadstar that “Antwerp and Zeebrugge’s combined throughput for 2019 is 13,536,064 teu, compared to 13,532,436 teu in 2024, which is a status quo”.

Alphaliner

Antwerp-Bruges rose one from spot from 15 to 14, while Hamburg sunk to 22 from 24 and Rotterdam was able to jump from 13 to 12 – largely due to Hong Kong’s decline from 11 to 13.

This would indicate that market share is being shifted to the Belgian port for European calls, rather than a structurally weak European market.

According to the eeSea database, Antwerp-Bruges currently hosts a stop for 131 services while Hamburg sees 93 and Rotterdam 153.

It noted that Rotterdam has a capacity of 21.5m teu and processed 13.8m teu in 2024, while Antwerp-Bruges utilised a larger portion of its 18.8m teu capacity last year, handling 13.5m teu.

The Port of Antwerp-Bruges told The Loadstar that the reason why it outperforms Rotterdam over this period is due to its diversification over different trade lanes, whereas Rotterdam has a strong orientation on Far East trade lane, and the fact that Rotterdam had a significant exposure to Russia-related containers which are now sanctioned.

However, Chinese ports continue to dominate the ocean-shipping supply chain, and they now make up one third of the top 30 by number, and half by throughput.

Unsurprisingly the number one port by throughput was Shanghai, although it was unable to extend its lead over second place Singapore, with the two ports currently locked in a difference of some 10m teu, according to Alphaliner.

Shanghai’s growth from the previous year was 4.8% while Singapore recorded 5.4% growth.

Ningbo-Zhoushan, however, was able to “clearly establish” itself in third place, having increased throughput by 11.3% from 2023, and Shenzhen managed to retain its fourth spot after being temporarily overtaken by Qingdao in the middle of the year.

“As a result, there were no changes in the rankings in the top 10,” said Alphaliner.

“The world’s top 30 container ports recorded a collective 7% increase in throughput in 2024, boosted by a surge in traffic in China, the US and the Indian sub-continent,” it summarised.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article