Ex-Schenker/DSV leader rumoured to join DHL Group

Watch out

KNIN: UPSIDEJBHT: STRONG TRADING UPDATE JBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'

KNIN: UPSIDEJBHT: STRONG TRADING UPDATE JBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'

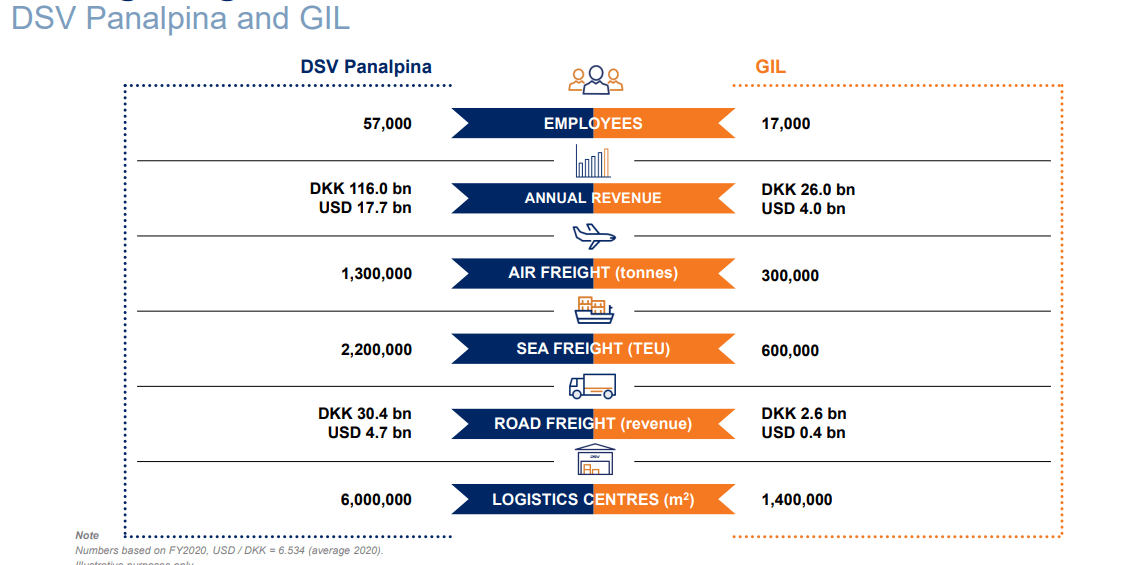

It’s big news that will shock no one. Some two years after DSV leapt into the list of forwarding superstars with its bold acquisition of Panalpina, it is now adding some $4bn to annual revenues with the acquisition of Agility’s Global Integrated Logistics (GIL).

It’s a new twist in an old tale: you may remember March 2019 when Panalpina’s shareholders flirted with the “fantastical” idea of buying Agility, instead of being folded into DSV, helpfully raising the Danes’ price in the process.

Agility rather enjoyed the dance, with then-chief executive of Agility GIL, Essa Al-Saleh saying the process had “whetted its appetite”.

For its part, DSV said this morning in a conference call that the acquisition was “an excellent strategic match”, adding significant volumes to its air and sea business. It said the corporate culture, as well as the similar asset-light business model would fit well. And geographically it works: Agility’s strength is in the Middle East and Asia Pacific, with a particular focus on emerging markets.

DSV said it plans to consolidate infrastructure, operations, administration and logistics facilities – but there was no word on possible job losses. DSV has some 57,000 staff, while Agility comes in at 17,000. In fact, DSV declined to disclose what synergies might be available.

DSV Group chief executive Jens Bjørn Andersen said in a statement: “GIL and DSV are an excellent match, and we are proud that we can announce our agreement to join forces. The combination of our two global networks will provide us with the opportunity to offer our customers an even higher service level.

“GIL’s strong market position in APAC and the Middle East complements DSV’s network well and will support our long-term value creation ambitions. Our two groups already share a culture of entrepreneurship and local ownership, and we look forward to welcoming GIL’s talented staff to DSV.”

It’s a 100% share deal, with an equity value of some $4.1bn and enterprise value of $4.2bn. A “simple” majority of Agility’s shareholders must agree and the deal is expected to be completed in the third quarter. DSV will nominate an Agility designee to DSV’s board.

DSV said the deal would give it a 4%-5% total market share, propelling it from number five in the freight rankings to number three, between Kuehne + Nagel and DB Schenker.

There will have been some serious due diligence relating to the acquisition. At the time of Panalpina’s interest in Agility, questions were raised over the lack of transparency in the Kuwaiti-headquartered company.

Mr Al-Saleh told The Loadstar at the time that the process had taught the company a few lessons.

“It’s not our intention to be murky and we have made steps to make it simpler. We are engaging with investors.

“We break down information on GIL – but we could do a better job. The Panalpina talks highlighted that we could be crisper in describing our business.”

While an Agility-Panalpina tie-up was blocked by by DSV’s Panalpina offer, Mr Al-Saleh expressed a view still widely held in the industry: “You have to give DSV credit – it is experienced and clearly doing something right.”

The announcement rather overshadowed DSV Panalpina’s first-quarter financial results. The group enjoyed a 21% rise in gross profit to Dkr7.78bn ($1.2bn), while ebit before special items rose 106% to Dkr3.06bn. Its Air & Sea division saw ebit rise 126% to Dkr2.4bn. But DSV’s air business saw a 7% volume decline, against a 5%-7% market growth, as it continues to be impacted by discontinued Panalpina activities. DSV said on a like-for-like basis its volumes would have grown 3%. Luckily, “the continued lack of capacity is keeping yields at extraordinary high levels”.

In sea too, DSV’s volume growth was nothing to write home about, at 1%. It said the growth was driven by Asian exports, and that there was “significant yield improvement”.

Revenues in road grew 3% to Dkr8bn but ebit jumped 57% to Dkr403m. Its solutions arm saw revenues up 9% to Dkr3.6bn.

Overall, it was a strong showing. Group revenues rose 28% to Dkr33.6bn, while first quarter profit came in at Dkr2.3bn.

Mr Bjørn Andersen said: “Today, we are proud to announce our agreement to unite with Agility’s Global Integrated Logistics. The combination of our two groups is a perfect match, and Global Integrated Logistics will add around 23% to DSV Panalpina’s annual revenue and strengthen our global network, especially in the Air & Sea division.

“On an eventful day, we are also happy to report 106% growth in ebit before special items in the first quarter of 2021 and an upgrade of the financial outlook for full-year 2021. The strong earnings growth in Q1 was driven by good performance in all business areas, and we benefit from cost discipline and the full-year impact from Panalpina synergies.

“The markets in air and sea are characterised by strong demand and tight capacity, and it takes an extraordinary effort by our staff to find good solutions for our customers under these challenging market conditions,” he added.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article