Brazil to allow shipping lines to bid for Santos Tecon10 terminal

The Brazilian government has put forward proposals to allow container shipping lines to bid for ...

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

Let me make my position clear from the start: I believe that the way Maersk is underestimating certain risks, while overstating its achievement, is near-sensational. While its latest trading update could sound reassuring to the bulls, for me it didn’t change the complexity of a corporate situation that remains critical.

Our team was on the call that followed its trading update last week, and was favourably impressed by the enhanced performance of the Danish group – it could have been much worse.

My colleague, Mike Wackett, soon identified the key value drivers, pointing out that the numbers were significantly better than expected. Not only did Maersk Line manage to beat consensus estimates, but Maersk Oil is now positioned to break even, with oil prices hovering around $40-45 a barrel from $45-55 previously.

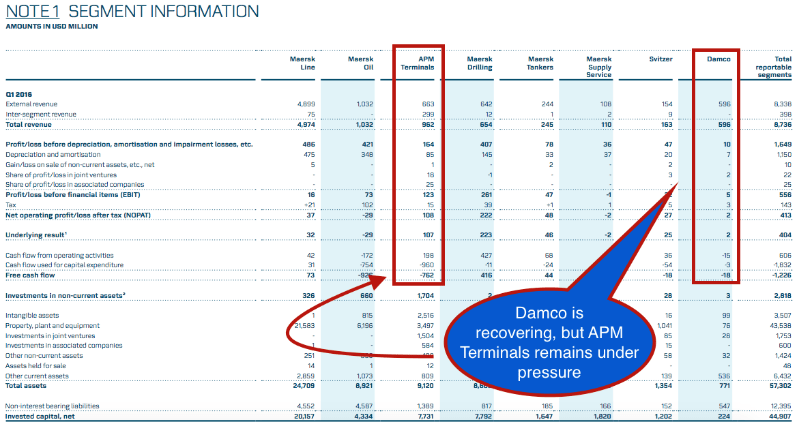

The devil is in the detail, however: perhaps the most interesting feedback we got from management on peripheral assets spanned Damco and APM Terminals – both of which deserved a mention, but for very different reasons.

The former is on the path to recovery and remains profitable after a turnaround that eventually paid dividends in 2015. But the performance of APMT was underwhelming, and was overstated by management, with chief executive Nils Andersen saying the group was only “a little bit disappointed” with APMT – still “a very profitable business”.

Source: AP Moller Maersk

APM Terminals

Maersk says APMT “now expects an underlying result below 2015 ($626m), due to reduced demand expectations in oil producing emerging economies”.

APMT sought strategic ties with Russia’s Global Ports in the past, bending certain unwritten rules for the unit – it prefers to take full control of the assets it targets rather than minority stakes. However, Russia is a long-term game, and so far consolidation in the country hasn’t played out as management expected.

In addition, global demand remained weak, especially in Europe, while the slowing Chinese economy and low oil prices continued to weigh on profitability.

“Being largely dependent on raw material exports, many economies in Latin America and West Africa, where APM Terminals has significant activities, continue to see declining growth and foreign trade,” Maersk noted.

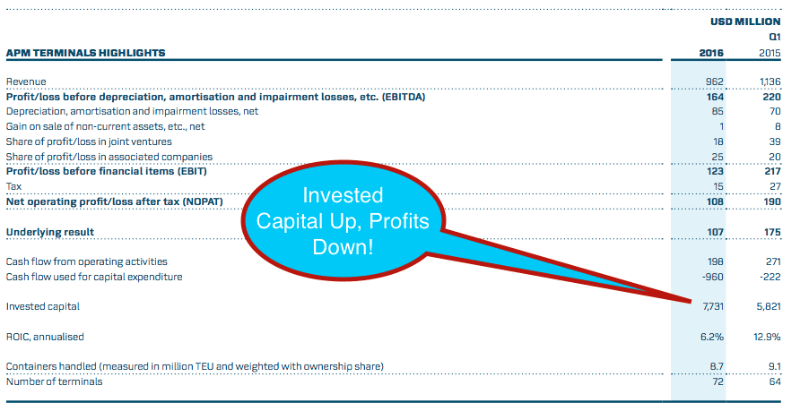

While the number of terminals has risen to 72, from 64 in Q1 15, containers handled – measured on ownership share – fell from 9.1m teu to 8.7m teu.

Decreased volumes on the westbound Asia-Europe tradelane impacted terminals in both China and Europe in a global container market that grew by 1.4% in the first quarter, according to Drewry estimates, with some regions “showing modest growth of 3-4% (North America and Middle East/South Asia), while markets declined in Northern Europe and West Africa”.

APM Terminals reported ebit of $123m, and currently represents a nice profit pool among its portfolio of assets – given that only Maersk Drilling, among other group assets, generates higher core operating earnings ($261m in the first quarter), and absorbs the same amount of invested capital ($7.7bn).

Source@ AP Moller MAersk

However, while APMT’s operating income plunged 43% from $216m year-on-year, the most problematic aspect of the business is the amount of cash that it burned in the first quarter, as investment is seen as a key value-driver for its long-term prospects.

Cost-saving initiatives contributed to earnings, but with quarterly capex at $960m and operating cash flow at $198m, APM Terminals reported $762m in negative free cash flow (FcF) in the first quarter alone, which was pretty close to the $926m negative FcF attributed to Maersk Oil. That compares with positive unit FcF of $49m one year earlier, when the amount of invested capital, though, was about $2bn lower, at $5.8bn.

Investment

During the quarter, APM Terminals wrapped up the acquisition of Spanish Grup Marítim TCB’s port and rail interests.

“APM Terminals has yet to receive regulatory approval related to three of 11 terminals under Grup Marítim TCB,” it added, but has decided to press ahead with the deal given that the remaining terminals constitute less than 5% of the enterprise value of the acquisition package.

The deal adds eight ports with a combined 2m teu equity-weighted volume to APMT, which also signed an agreement to develop “a new transhipment terminal at the Tangier Med 2 port complex, with an annual capacity of 5m teu”.

When it launches in 2019, it will be the first automated terminal in Africa and the total investment is expected to be around $900m, with APMT’s share being 80%. It already operates the APMT Tangier facility at Tangier Med 1 port, which started operations in July 2007 and handled 1.7m teu in 2015.

There could be short-term pain for long-term benefits, if its strategy is right – but the problem is that Maersk might have to accelerate cost savings elsewhere if APMT continues to burn cash, and options are thin on the ground.

Damco

Hanne B Sørensen has led Damco since January 2014, and under her stewardship the forwarder has started to shine again. Its turnaround is by no means over, but all the signs seem to point to a sustained recovery.

Damco made a quarterly profit of $2m, versus a loss of $9m one year earlier, with its ROIC coming in at 3% against -11.2% in the previous year. The division was confirmed to be on the right track in early 2016, following a year during which it was mildly profitable after two years of losses.

Its quarterly result was mainly driven by cost-cutting and growth in contract logistics, Maersk said, with a “focus on driving customer service improvements, delivering on cost optimisation plans and increasing productivity”.

The division is shrinking in terms of revenues, down to $596m from $683m year-on-year, but was in the black and absorbs a very small amount of capital.

Talking of which, we should also mention market reports that suggest Maersk’s cash pile gives it plenty of options with regard to capital deployment strategies and M&A.

M&A and away

There’s talk that Maersk will join the consolidation game in shipping, given that it has cash and equivalents and undrawn facilities of $11.8bn.

A bolt-on deal could make sense, but Maersk has recently decided to err on the side of caution and it would seem wise to maintain a low profile in terms of capital deployment in this environment.

My initial reaction to the surge in its valuation last week – its shares rose over 6% on Wednesday after the results were out – was to suggest internally that the price movement was likely going to be short-lived, just as happened in the third quarter of 2015. After all, here are some more interesting figures:

On the bright side, it looks like return on invested capital is bottoming out at about 3%, and remains unchanged quarter-on-quarter, although it sits some 11 percentage points below the 13.8% level it recorded one year earlier. In terms of valuation, we are back to where we were at the beginning of the year, given that its stock price is up 4% since January.

Finally, here are a couple of things to like outside the headline numbers:

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article