Analysis: Mærsk lines up Bremerhaven as its new German jewel

Colour code all of them now

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

Hamburg’s main container terminal operator HHLA finds itself at critical juncture in its business life cycle.

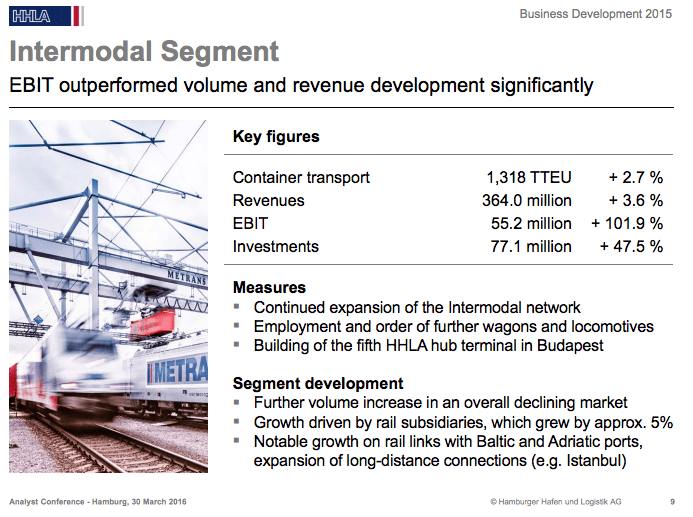

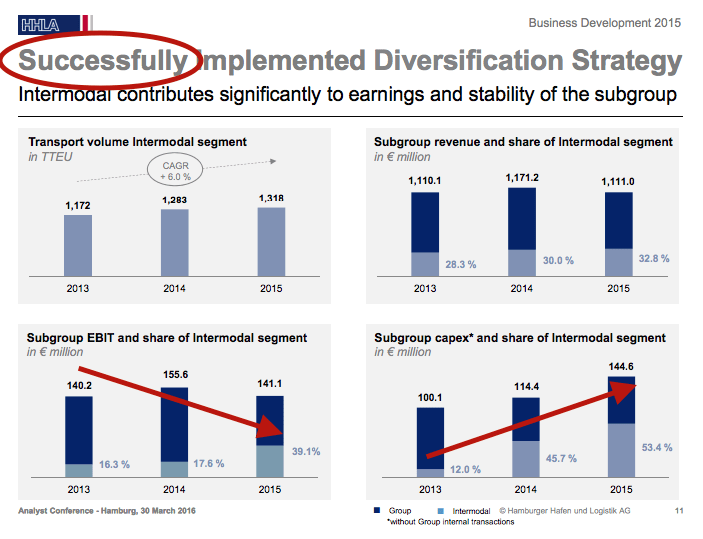

A mature business, with 131 years of glorious history, it must now continue to diversify from its core container operations, committing more capital to the intermodal activities that delivered the best performance across the group in 2015.

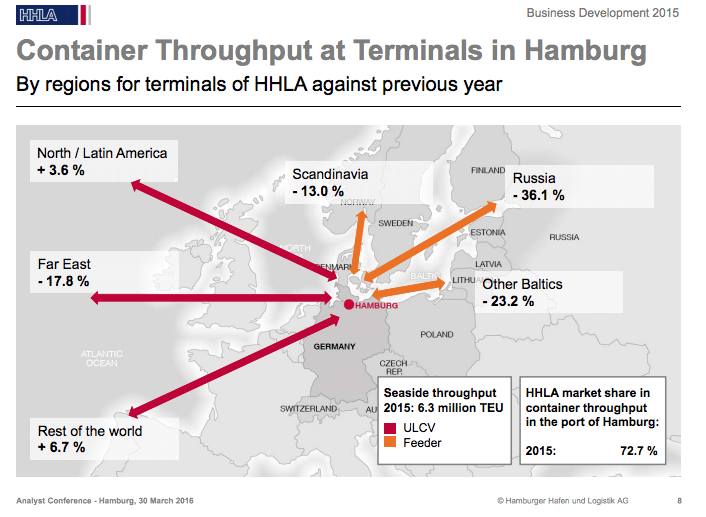

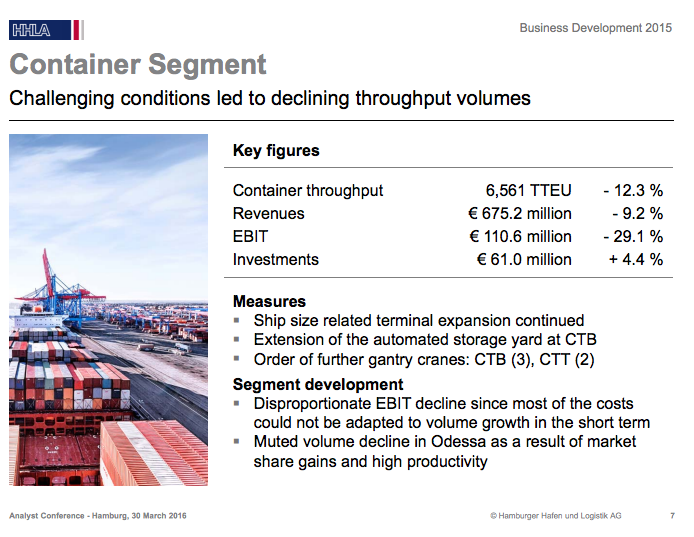

The container division still generates almost 60% of turnover, but is a drag on performance and relies on throughput at terminals in Hamburg, as the chart below shows.

The unit succumbed to the limp trading on Asia-Europe services and continued to be hit by the sanctions on imports to Russia in 2015, with sales hitting €675m, down 9.2% year-on-year – the lowest level of revenue since 2012.

That is the headline number, and neither does it look good at cash flow level, with container handling Ebitda down 20.8% to €195m. What makes things even worse is the marked deterioration of Ebitda margins, which dropped 420 basis points to 29% last year.

Lower cash flow profitability in its core business makes debt repayments heavier, narrows its funding options in future budgeting because taking on more debt either to finance organic expansion or the purchase of strategic stakes to boost its growing intermodal exposure might eventually undermine its dividend policy, which is the main attraction for investors nowadays.

Prove yourself

In a press release dated 30 March, and headed “Port and transport logistics – a strategy that’s proven itself”, HHLA stated that the executive board and the supervisory boards were proposing a significantly higher payout to shareholders, currently at over 60%.

However, I believe it could be as soon as this year that it might have to make the hard choice between cash returns and higher investment in non-core units.

On the bright side, there remains fat on the bone in terms of operating costs – which were flat year-on year – before the dividend is chopped, although bank loans and finance leases amount to €370m, which implies a rising net leverage position hovering around 1x. That is its highest level in recent years.

Significantly lower cost of materials, the “decrease is mainly related to cost structure changes resulting from the increased use of the company’s own traction, which more than offset the opposing effect of growth in the material-intensive intermodal segment”, contributed to a rise in net income to €96m, of which €30m is attributable to non-controlling interests rather than to the shareholders of the parent company.

Also, thanks to lower tax expenses, earnings per share are rising in the double-digit territory on a constant share count, but cash flows per share are falling while heavy investment is rising, and the trend is clear: more will have to be invested in intermodal, because investment is driving income growth.

In a market where container throughput is unlikely to recover in the short-term, as HHLA acknowledges, management must find alternative solutions to restore confidence in its corporate story, which at the time of its 2007 IPO was sold to investors by JP Morgan and Citi, whose analysts’ “pinpointed a market value of up to €3.6bn”, Reuters reported at the time.

“Since its IPO, there has been no cessation in the interest in HHLA displayed by international investors, among them virtually all the well-known investment funds,” HHLA said in its 2009 annual report.

Its current market value stands at less than €1bn. If the right offer emerges, management would do well to take the money and run, in my opinion.

The fall

The plunge in its share price – down 31% in the past 12 months alone – has pushed its forward/trailing yield well above historic trends at over 4%.

This signals plenty of downside risk both in its valuation and in its dividend policy, and existing investors have to gauge whether management is actually capable of pursuing an even more aggressive intermodal expansion to propel shareholder value, taking the view that it is worth holding onto shares at their current multi-year lows.

Certainly, the stock does not look like a bargain based on a top-down approach, while disturbing signs also come from its growth trajectory, earnings multiples as well as cash flow and price-to-book ratios.

It is of paramount importance, however, that its valuation doesn’t collapse from its depressed level of €13.5 a share – its IPO was priced at the top end of a €43-53 range – because fresh equity may be needed either to finance new investment or to keep capital ratios in order if net leverage keeps rising.

Operating cash flow declined from €233m to €195m on the back of falling operating profits and lower cash inflows from working capital management – the latter, in particular, is a pretty bad sign for a company chasing diversification just when core margins are under pressure.

HHLA’s free cash flow – cash resources available either for dividend payments or the redemption of existing loans – declined 45% year-on-year from €119m to €65m, primarily as a result of lower Ebit, a decrease in trade and other liabilities, and higher cash flow from investing activities.

Its free cash flow yield (fcf/market cap) is a rich 7%, but that’s only because its market value has plummeted – and now it is time to keep a close eye on cash balances. Its gross cash position dropped by €20m to €165m in 2015.

Buying time

I believe the next 24 months will be particularly important in its turnaround.

In fairness, a cash call is not around the corner, and HHLA could also simplify its corporate tree to raise funds if it needed to invest more heavily in intermodal.

For example, it could spin off its smaller real estate and logistics assets, but this would just buy some time if underlying margins in its terminals unit do not bounce back.

Another alternative would have been to adopt a more conservative dividend policy while promoting a corporate story centred on the growth potential of intermodal, but management thinks HHLA remains a safe place for income investors.

“HHLA will continue to pursue its yield-orientated dividend distribution policy which aims to pay out between 50% and 70% of net profit for the year after non-controlling interests in the form of dividends,” it said.

There remain bright spots out there for the bulls, of course, but I have also noticed that revenue of €131m from a single client “exceeds 10% of group revenue and relates to the container and intermodal segments”.

I’m not sure that HHLA is as safe as it appears.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article