Box ship attacked, Hormuz shut again, Middle East rates sail past pandemic peak

Gulf importers and their forwarders are once more turning to Middle East landbridge routes after ...

HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISHCHRW: POSITIONING AHEAD OF EARNINGSAMZN: IN THE NUMBERSAMZN: PEOPLE MATTER UNTILVW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP

HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISHCHRW: POSITIONING AHEAD OF EARNINGSAMZN: IN THE NUMBERSAMZN: PEOPLE MATTER UNTILVW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP

Airlines are redeploying freighter capacity in search of higher yields, as weak demand fails to bring down air cargo rates in a market still distorted by disruption.

Despite falling volumes, pricing remains elevated, with carriers prioritising profitable lanes and reliable routings rather than restoring pre-crisis networks.

Source: Rotate. Freighters and widebody pax

Capacity is beginning to return, but not evenly. Growth is concentrated in the Middle East and South Asia, while other regions lag, leaving key corridors still constrained.

That imbalance is shaping airline behaviour.

Source: Rotate – freighters only, week on week.

Freighter data shows capacity being redeployed selectively, with gains in intra-Asia and Middle East markets contrasted by weaker transpacific flows. Rather than rebuilding networks, operators are shifting lift toward lanes offering stronger returns.

At airline level, the divergence is even clearer. Major operators are pulling back: Lufthansa cut freighter capacity by roughly a third week on week, with Saudia and Ethiopian down by around 10% and 8%, respectively. Growth is being driven by integrators, select Gulf carriers, and a rise in ad hoc charter activity.

The result is a more opportunistic market, with capacity chasing yield rather than demand.

That is also evident in shifting tradelanes.

Source: Rotate, freighters only, week on week

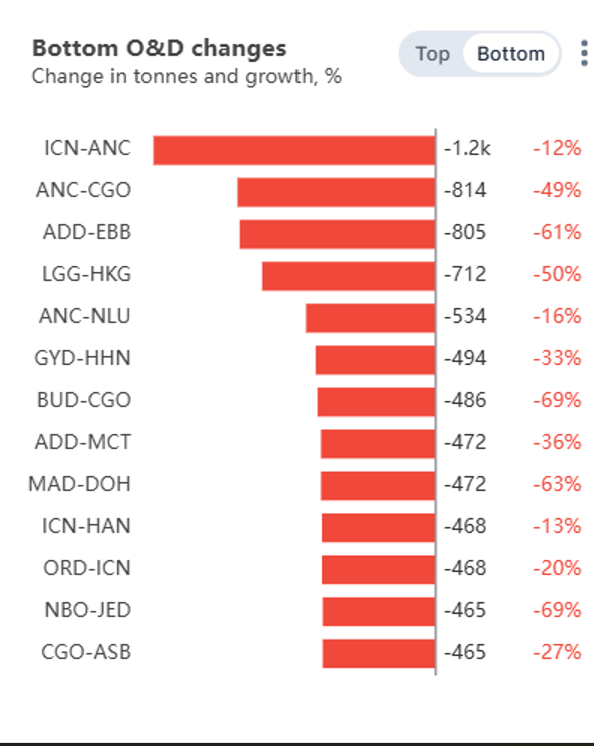

Middle East-linked routes such as Hong Kong–Doha and Amsterdam–Doha are rebounding as airspace restrictions ease and hub activity begins to recover. But transpacific flows are weakening, with sharp declines on lanes including Incheon–Anchorage and Anchorage–China.

The sharp fall in Anchorage flows appears to reflect structural rerouting, rather than a simple shift to nearby alternatives such as Fairbanks.

While some carriers have used alternative technical stops in Alaska, due to fuel supply concerns, the data suggests a broader shift from Anchorage as a transpacific cargo hub, with airlines reducing hub-based flows rather than eliminating stopovers altogether.

At the same time, bellyhold capacity is gradually returning. Gulf Air has resumed operations from Bahrain, following the reopening of airspace, signalling a cautious restart of Gulf hub activity, although services remain limited and partially supported via Dammam.

Even so, the return of capacity has yet to translate into lower prices.

Industry data shows air cargo rates continuing to edge higher, even as volumes decline. WorldACD figures for the week to 12 April put global spot rates up a further 3% week on week, at $3.76 per kg, leaving them 37% higher year on year, and more than 40% above their level at the end of February, before the escalation in the Middle East.

The rise comes despite a 6% drop in global tonnages over the same period, underlining the extent to which pricing is being driven by constrained and misallocated capacity rather than underlying demand.

Regional trends point to the same imbalance. Rates from North America rose 6% week on week, while Asia Pacific edged up a further 2%. From the Middle East and South Asia, rates eased slightly on the week, but remain sharply elevated – up around 66% year on year – reflecting the ongoing disruption to capacity in the region.

Daily TAC Index data suggests the pattern is continuing, with Asia–Europe lanes holding firm or edging higher, and India–Europe rates strengthening, while transpacific pricing shows signs of softening.

Instead, pricing is being supported by a combination of constrained capacity on key lanes, ongoing ocean freight disruption pushing cargo into the air, and persistently high operating costs.

Fuel remains a key factor. Although jet fuel prices have shown some signs of stabilisation, surcharges – based on data from Hong Kong – remain near peak levels, reflecting both lagging adjustment mechanisms and continued uncertainty over supply.

With the ceasefire between Washington and Tehran still fragile, few expect a rapid return to normal network conditions.

Catch up with today’s News in Brief podcast, featuring Drewry’s Chantal McRoberts, to break down the latest on container shipping

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article