Air cargo in new balancing act as rates ease and fuel costs climb

Air cargo carriers are facing an increasingly challenging market, with spot rates beginning to cool, ...

WTC: NO LUCKCHRW: 'NUCLEAR VERDICT'DSV: DEEP CUTKNIN: UPGRADEDKNIN: AI BENEFITSKNIN: NOT WORTH ITPLD: DEAL TIMEKNIN: CONF CALL CLOSING KNIN: PRICING POWER KNIN: MARKET SHARE GAINS IN ROAD KNIN: AI-RELATED COST INFLATION OUTLOOKKNIN: APEX LOGISTICS IPO UPDATEKNIN: QUESTION TIMEKNIN: 'COST REDUCTION PROGRAMME IS ON TRACK'KNIN: CFO REMARKSKNIN: MONETARY IMPACT FROM AI KNIN: AI UPSIDEKNIN: STRONG ROAD UNIT DELIVERY KNIN: AIR LOGISTICS SHINES

WTC: NO LUCKCHRW: 'NUCLEAR VERDICT'DSV: DEEP CUTKNIN: UPGRADEDKNIN: AI BENEFITSKNIN: NOT WORTH ITPLD: DEAL TIMEKNIN: CONF CALL CLOSING KNIN: PRICING POWER KNIN: MARKET SHARE GAINS IN ROAD KNIN: AI-RELATED COST INFLATION OUTLOOKKNIN: APEX LOGISTICS IPO UPDATEKNIN: QUESTION TIMEKNIN: 'COST REDUCTION PROGRAMME IS ON TRACK'KNIN: CFO REMARKSKNIN: MONETARY IMPACT FROM AI KNIN: AI UPSIDEKNIN: STRONG ROAD UNIT DELIVERY KNIN: AIR LOGISTICS SHINES

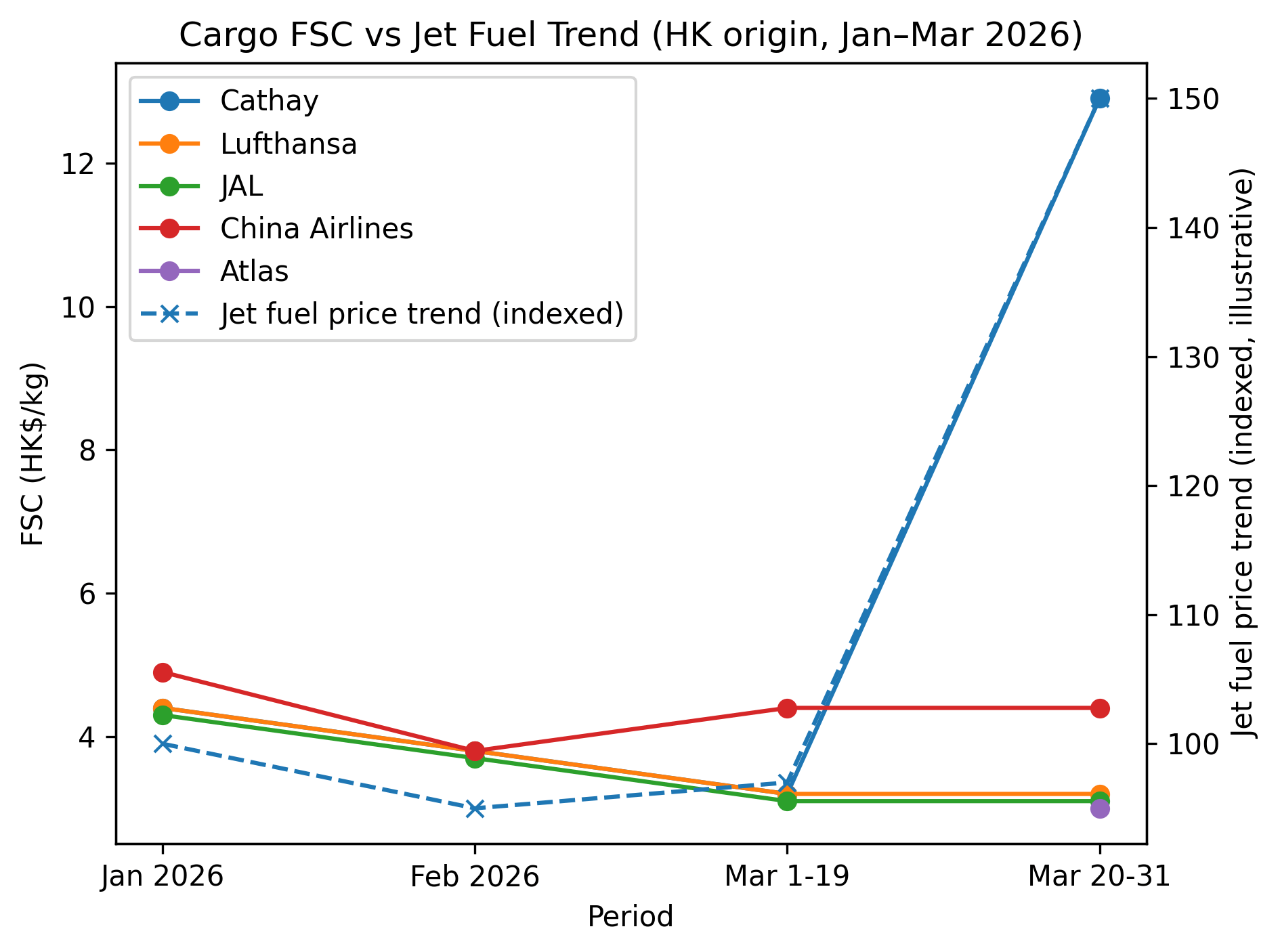

Cargo fuel surcharges jumped sharply in late March as jet fuel prices spiked – but not all airlines followed.

New data from Hong Kong, where carriers publish cargo fuel surcharge (FSC) levels, shows a widening gap in pricing responses, with some airlines holding steady while others pushed through dramatic increases.

The divergence comes as parts of the industry face renewed exposure to fuel volatility after years of scaling back hedging programmes.

Through January and February, FSCs moved largely in lockstep. Long-haul surcharges across major carriers clustered tightly:

Into early March, the pattern held, with most airlines sitting around HK$3 to HK$4/kg. For several months, FSCs appeared to behave as intended, tracking fuel prices and converging across carriers.

Then it all changed. From 20 March, Cathay Cargo raised its long-haul FSC from HK$3.2/kg to HK$12.9/kg. Other airlines did not follow.

Within days, long-haul FSCs ranged from roughly HK$3/kg to nearly HK$13/kg – a more than fourfold spread in the same market.

According to IATA data cited by Cathay Cargo, the global average jet fuel price rose from $95.95 per barrel in the week ending 20 February to $197.00 per barrel by 20 March, driven by both higher crude prices and a surge in refining margins.

Dominic Perret, director cargo at Cathay, said the situation had created “challenge and volatility” across the industry. “The surge in the price of jet fuel is placing considerable pressure on airlines around the world,” he said.

Despite that, the increase still fell well short of the jump seen in some surcharges, raising questions over how FSCs are set.

Dan Morgan-Evans, head of cargo for broker Air Charter Service, said the variation had become increasingly difficult to justify.

“Obviously we’re in the same boat as everyone else – oil prices are the major factor in our business right now,” he said. “But fuel surcharges vary significantly from carrier to carrier.”

He added that the link between costs and pricing was not always clear. “You would think a lot of airlines had hedged their fuel – perhaps they didn’t, or they’re using fuel price increases as an excuse,” he said.

“For us, it’s difficult. Customers understand what’s going on in the market, but it’s still a tough pill to swallow when previously contracted flights are suddenly hit with huge fuel surcharges.”

The divergence comes against a broader shift in how airlines manage fuel risk.

Over the past two decades, many carriers, particularly in the US, have scaled back or abandoned fuel hedging programmes. Southwest Airlines, once a leading hedger, formally exited hedging in 2025, arguing the strategy had become “expensive and unreliable”.

Critics say this reflects a misunderstanding of risk management. As The Loadstar Premium recently noted, airlines began treating hedging desks as profit centres rather than insurance policies, abandoning them when prices fell and derivatives appeared costly.

The result is an industry more exposed to sudden fuel shocks. With refining margins recently hitting levels last seen during the 2005 hurricane-driven crisis, some analysts warn airlines now face billions of dollars in additional annual fuel costs.

Cathay said hedging offered only partial protection in the current environment.

“Like many airlines, Cathay undertakes fuel hedging to manage price volatility. However, in 2026 our hedging covers only around 30% of the crude oil component and does not apply to the refinery component,” Mr Perret said.

“Fuel surcharges are another important mechanism to mitigate and recover a portion of our incremental fuel costs… we have had to increase fuel surcharges in response to the price increase in jet fuel.”

In theory, differing hedging strategies should lead to different cost outcomes.

European groups such as Lufthansa and IAG typically hedge a substantial share of near-term fuel exposure, often covering a majority of expected consumption over a 12–24 month horizon. Asian carriers, including Cathay Pacific, also maintain structured hedging programmes, although coverage varies. By contrast, US operators, thought to include Atlas Air, tend to hedge little or not at all, relying instead on contractual pass-through or market pricing.

In theory, this should translate into varying cost pressures. However, the Hong Kong FSC data shows no consistent relationship between exposure and pricing. Instead, the latest data suggests FSCs may also function as a flexible pricing tool.

In stable markets, airline behaviour converges, giving the impression of a standardised mechanism. But in volatile conditions, that consistency breaks down and differences become visible.

Some carriers adjust gradually, others move sharply, and some do not apply a separate surcharge at all.

So while FSCs may track fuel prices, they do not do so uniformly, or always proportionally.

As volatility returns to energy markets, and airlines take increasingly divergent approaches to managing fuel risk, that variability is likely to become more pronounced.

The question for shippers is no longer just where fuel prices are heading, but how airlines choose to respond.

Check out the new Loadstar Snapshot on who pays the bills:

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article