Box ship buying spree is over, says Braemar, lines must be more selective

The surge in orders for small and mid-sized containerships has largely addressed the structural capacity shortfall that ...

WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISH

WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISH

Container spot rates are showing “unusually early signs” of peaking, ahead of next month’s Chinese New Year (CNY) holiday, compared with how they typically behave.

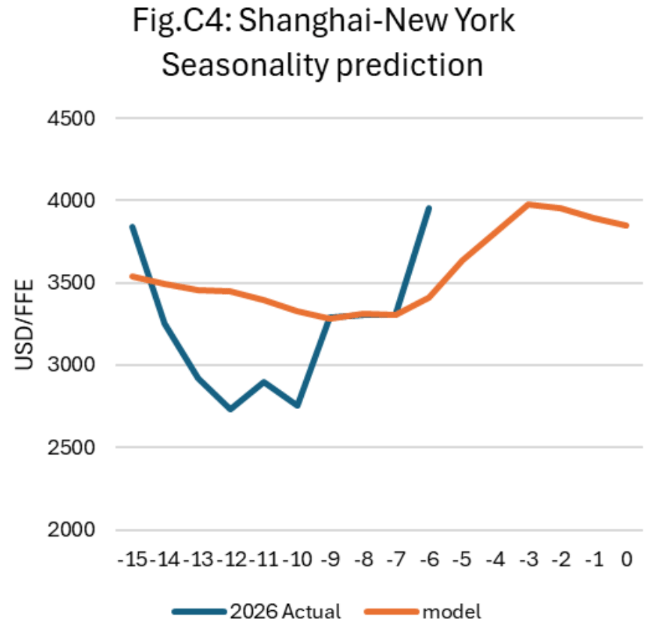

Recent analysis from Sea-Intelligence, using data from Drewry’s World Container Index (WCI) between 2013 to 2025, shows that, on the transpacific, to the US east coast, there was a well-defined seasonal structure where rates historically peak around two to three weeks before CNY, following a slack period between ten and six weeks previous to the holiday.

When compared with WCI data, Sea-Intelligence’s seasonality-based projection for 2026 shows the pre-peak slack period was weaker than normal, while the recent spike in rates exceeded what seasonality alone would suggest.

Source: Sea-Intelligence

“For this trade, it would therefore appear that either we have already hit the peak rate three to four weeks earlier than usual, or we are about to enter into an above-normal peak in spot rates leading up to CNY,” explained the analyst.

There was a similar picture on lanes to the US west coast, on which rates typically peak around three weeks before CNY. 2026 data shows a deeper slack season followed by a rapid climb that matches expected peak levels well ahead of schedule.

Source: Sea-Intelligence

On the Asia-Europe trades, seasonality is more pronounced. For Shanghai-Rotterdam, WCI data shows rates usually peak three to four weeks before CNY, with sharper post-peak declines.

And Sea-Intelligence noted that, while the slope of weekly increases in 2026 closely matched historical patterns, the ramp-up is occurring roughly two weeks earlier than normal. And Shanghai-Genoa mirrors this behaviour.

Source: Sea-Intelligence

“The data for all four trades shows that, from a seasonality perspective, we have already reached the expected apex rate prior to CNY,” said Sea-Intelligence.

“If this is the case, it means Asia-Europe is peaking two weeks earlier than usual and the transpacific is peaking three to four weeks earlier than usual. Should we therefore see further increases in the coming weeks, these will signal an underlying strength in the market above and beyond seasonality,” it said.

However, the analyst added that if spot rates should decline in the next couple of weeks, it means “we are past the peak”.

Indeed, maritime consultant Braemar said: “Freight markets have started the year on a firmer footing, but the key question now is how much of this strength will be sustained once Chinese New Year is behind us.”

The consultant noted that demand was now building ahead of the holiday and “freight markets have reacted swiftly”.

“Several GRIs have held, pushing spot rates sharply higher this week,” it said, but added that today’s levels remained around 35% to 40% lower than at the start of 2025.

“In other words, this represents a solid seasonal bounce, rather than a return to last year’s freight highs,” explained Braemar.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article