WiseTech defends DSV relationship, as CargoWise volumes rise 20%

In what has been a troubled week, WiseTech Global is seeking to reassure investors over ...

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

And so the forwarding consolidation chat continues. On Loadstar Premium today, we reveal speculation that CMA CGM, new proud owner of Ceva, is in talks with the French government over the possible acquisition of Geodis.

Geodis has said publicly it is looking for a slice of M&A action – but that it wanted to expand in Germany, the Netherlands, China and the US.

Currently owned by a French railway, could Geodis switch to being owned by a French shipping line? Is this the kind of M&A it was looking for?

CEO Marie-Christine Lombard has said Europe must eventually become “our second home market”, implying a different sort of tie-up – a shipping line would not provide the scale it is looking for, but a tie-up with Ceva might.

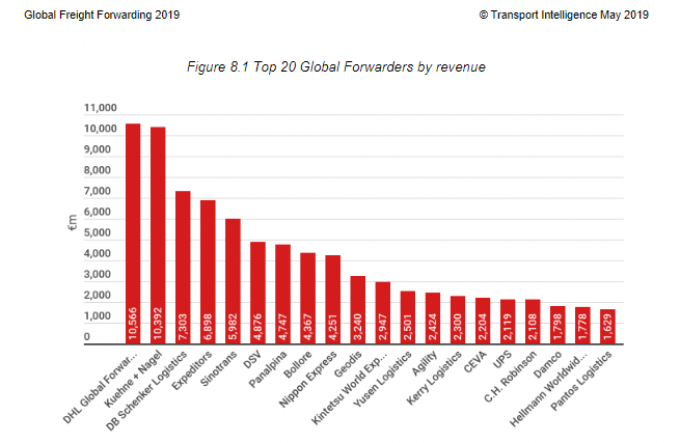

Meanwhile, Ti has done the maths, and suggests DSV Panalpina will account for 6% of the forwarding market after their merger is complete, according to its Global Freight Forwarding 2019 report, becoming the third largest forwarder by revenue, rivalling Kuehne + Nagel and DHL Global Forwarding.

As Ti notes, “the reasons for the merger are fundamentally not complicated. Panalpina’s profits, if anything, have fallen since 2014, while in contrast, DSV’s more than doubled”.

It adds: “DSV has grown through a combination of acquisition and organic growth. It has been highly successful at integrating its often large acquisitions rapidly. Therefore, it was logical that DSV continue this approach, while Panalpina was the right size and [is] reasonably complementary in terms of geographical and vertical sector positioning.”

Panalpina was, of course, also on Agility’s wishlist. The chief executive of Agility GIL told The Loadstar last week: “We were disappointed as there was strong logic behind it, and it would have created a lot [of value]. You have to give DSV credit – it is experienced and clearly doing something right.”

But he dismissed the idea that vertical consolidation was right for forwarders: “Our value proposition is that we sit in the middle, neutrally trying to connect the dots.”

Others suggest shareholding structures have no real market impact. And is there any impact on carriers from the M&A merry-go-round in forwarding?

“I haven’t seen any negative affect,” said Rick Elieson, president of American Airlines Cargo. “There may be changes in account management and some other things that change – but there is no angst.

“The forwarding market is still so fragmented.”

Ti’s Global Freight Forwarding 2019 report shows that globally, the top 20 forwarders account for 57.5% of the market. Consolidation has helped them to build scale and market share. When DSV Panalpina become one of them, the top five players will account for 27% of the market. And more M&A is likely, with both Geodis and Agility in the game.

“As the first half of 2019 draws to a close, the forwarding sector remains the focus of rumours about further acquisition activity by the larger forwarding companies,” said Nick Bailey, head of research at Ti.

“The rationale is generally economies of scale or the need for greater exposure to global markets, either geographic or vertical. Another rationale, less loudly articulated, is a fear of being left behind.

“With the new DSV Panalpina set to be a credible rival to both Kuehne + Nagel and DHL Global Forwarding in almost all markets, other large forwarders will be feeling pressure to keep up.”

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article

A.Kout

June 13, 2019 at 2:13 pmWell, will be interesting to see how a DSV can achieve the snyergies they have distributed with the Panalpina merger in a market

where almost every multinational has achieved in the 1 quarter of 2019 a tremendous decrease in available airfreight tonnages of 25-to 30%,

where according to the market, a very intensive fierce competition is going up as almost everyone is selling over price, which in turns does have an fantastic impact on the net profit, so the most forecast we see by the multis are heavily in doubt from our side.

Concentrating too much on general cargo which most Multis still do, is not really the best way of achieving better higher margins. Additionally if you speak with industry shippers, the service quality most Multi´s today render is not in line with their expectations. Standardisation is not really everything, decision makers have to rethink otherwise …..

regards

A.Koût

Anonymous

June 18, 2019 at 8:04 amDachser SE is missing in the stats.

5.6 Billion Euros rev