Battle for freighter capacity intensifies as airlines reshape networks

A cluster of shocks is forcing freighter operators to finely balance their global capacity – ...

VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTIONDHL: NEW HIGH TARGET ON THE STREET DSV: EXPECTATIONS RUN HIGH KNIN: DHL GUIDANCE UPGRADE READ-ACROSSKNIN: NEW OPENINGGM: TECH UPSIDEAMZN: BIG DEBT FUNDING ON ITS WAYDHL: 'STELLAR EXPRESS'DHL: UPDATEDHL: STRONG PRELIMINARY UPDATE CHRW: STILL VERY BEARISH

VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTIONDHL: NEW HIGH TARGET ON THE STREET DSV: EXPECTATIONS RUN HIGH KNIN: DHL GUIDANCE UPGRADE READ-ACROSSKNIN: NEW OPENINGGM: TECH UPSIDEAMZN: BIG DEBT FUNDING ON ITS WAYDHL: 'STELLAR EXPRESS'DHL: UPDATEDHL: STRONG PRELIMINARY UPDATE CHRW: STILL VERY BEARISH

M&A is expected to increase among the fragmented forwarding sector this year, with several companies announcing their intention to expand geographically.

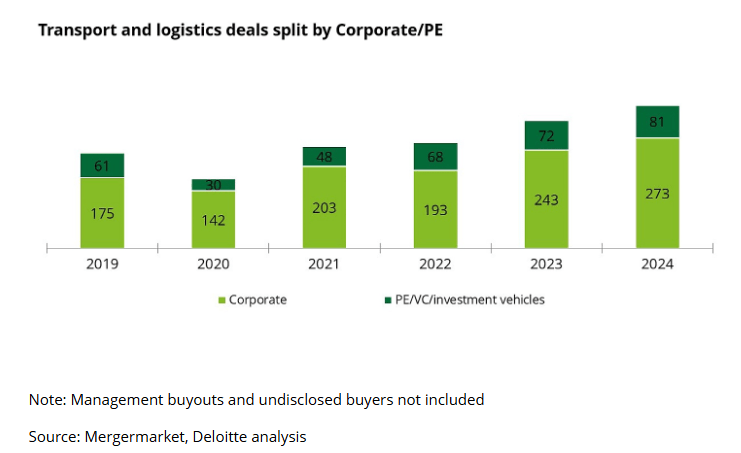

Last year, M&A activity in transport & logistics increased for the first time since 2021, albeit with fewer, higher value deals. Corporate deals were up 12%, and accounted for 75% of deals last year – a trend which Deloitte said in its May M&A report is likely to continue.

“The count in deals were primarily driven by corporates entering new geographies, building scale and enhancing capabilities, as well as pent up demand from PE contributing to higher deal activity…

“Large service providers are also building deeper sector specialisms making them indispensable to their customer base.”

Forwarders appear to agree – particularly as the gap between the ultra large companies and others begins to widen. The industry is still highly fragmented – even after its takeover of DB Schenker, DSV still only has 6 to 7% of the global market share.

Geodis is one such forwarder that wants to retain its position in the market.

“Our mission is to stay among the top 10 and to be a global provider,” said head of global forwarding, Henri Le Gouis. “Our three pillars are road services, contract logistics, and air and ocean. And we want to base our growth strategy on these three pillars, when we think that an acquisition can give us access to a more comprehensive mapping of each of our goals.

“Where acquisitions make sense to help and fuel our strategy, we use them.”

He added that shareholder SNCF is supportive of the strategy: “We’ve always had the support of our shareholders when it came to acquisitions that we estimated to be profitable. But in no case will we be only focusing on one business. We will focus on three pillars.”

Dachser is another forwarder eyeing inorganic growth.

“We are definitely not finished with M&A yet. In the last years we heavily invested in Europe, mainly in our food logistics,” said Burkhard Eling, CEO.

“So now in Europe we are really well established.”

As a result, Dachser is looking beyond Europe for its next steps.

“We have markets outside Europe that are growing faster than Europe. Even though we are in the majority of the markets, our footprint may not represent the size of the market, and this is what we are currently looking for.”

He added that it was too early to announce any specific deal – but it is looking at North America and southeast Asia.

Mr Le Gouis added: “It’s just a matter of opportunities. I think there are some fast-growing markets. I think we need to look carefully at more regional supply chains in the future; we are thinking especially of Eastern Europe, India, southeast Asia and Latin America. There is still some room for growth in this business.”

In terms of verticals, he said, automotive remains strong. “It’s a global supply chain. No car will be fully assembled in only one country. You will see spare parts traveling all over the world. For us, it’s still an industry that will need some value added. This is also true for project logistics, which is key to us, because there is such a demand for energy.”

But there is one vertical that doesn’t hold much interest for Geodis: ecommerce.

“As far as air and ocean are concerned, we sometimes deal with some air freight for ecommerce but it’s limited. It’s not a strategic development for us.”

Dachser, which has invested heavily in its food logistics business, is still looking to enlarge its network.

However, explained Mr Eling, food logistics is relatively regional and depends on temperature zones, such as ambient, chilled, frozen and so on.

“They have different equipment needs that you have to establish, and this is exactly what we are looking at right now, in which markets we want to be.

“Food is a much more stable business. It is competitive, but in the end you need to feed 82m people in Germany. This is a good diversification.”

Dachser also specialises in DIY, chemicals, life science, healthcare and fashion, but for non-European growth, high-tech and semi-conductors is strong, he said.

M&A this year won’t only be corporate bolt-ons – private equity will also be in the mix, said Deloitte.

“PE-backed deals in the sector followed the wider European trend, increasing by 13% year on year to 81 in 2024, with PE firms investing in a variety of subsectors including haulage and transport, couriers and parcels, warehousing and third-party logistics.

“This could be due to PE groups capitalising on the continued disruption to the logistics industry and relatively weak market conditions (eg higher interest rates) in 2024 which have enabled more acquisitions at favourable terms,” it noted.

This article is © The Loadstar. Reproduction, rewriting, or derivative use requires a license. Contact [email protected] for licensing enquiries.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article