Hormuz 'definitely shut', landbridges under pressure – TIR to the rescue?

With tentative hopes of a reopening of the Hormuz Strait dashed by the wave of ...

HON: DEALS ON THE MENUEXPD: NEW RECORD XPO: THE REBOUNDCAT: PAYOUT UPDHL: LIGHTHOUSEMAERSK: ANOTHER UPGRADEFWRD: HEALTHY CORRECTION R: RYDER CEO SAYS R: AMAZON LTL ANNOUNCEMENTPLD: EV INFRASTRUCTURE PUSHDHL: RAMPING UP 'NEW ENERGY LOGISTICS' GXO: NEW WINAMZN: LTL SERVICE UPDATEGM: ENERGY PROVIDER MODEL

HON: DEALS ON THE MENUEXPD: NEW RECORD XPO: THE REBOUNDCAT: PAYOUT UPDHL: LIGHTHOUSEMAERSK: ANOTHER UPGRADEFWRD: HEALTHY CORRECTION R: RYDER CEO SAYS R: AMAZON LTL ANNOUNCEMENTPLD: EV INFRASTRUCTURE PUSHDHL: RAMPING UP 'NEW ENERGY LOGISTICS' GXO: NEW WINAMZN: LTL SERVICE UPDATEGM: ENERGY PROVIDER MODEL

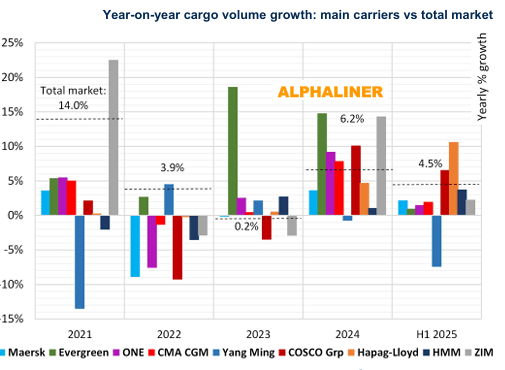

Hapag-Lloyd and Cosco have sailed ahead of average container market growth, leaving their liner counterparts in their wake.

Against Container Trade Statistics’ (CTS) global volume growth figure of 4.4% year on year in August, The two were the only major carriers to beat the market average, reported maritime analysts at Alphaliner.

The German carrier lifted volumes of 6.7m teu over the first half of 2025, an 11% increase on H1 24.

Just after Hapag-Lloyd published its Q1 carried volumes, showing 9% growth year on year, double the CTS market figure of 4.2%, CEO Rolf Habben-Jensen told The Loadstar: “I think that’s largely because of the network we have right now.”

“We have higher schedule reliability, which has two big benefits: one that our on-time delivery is much better; but we also sail every week,” he explained.

“In previous years, we’ve had to blank quite a lot of sailings because of the delays. Now we don’t do that, so that automatically creates some growth, because instead of having, let’s say eight voyages in ten weeks, you now have ten in ten weeks and, almost automatically as a consequence of that, you’ll see above-average growth.”

Indeed, Alphaliner reported: “The German carrier had to blank fewer sailings in 2025 after switching from THE Alliance to Gemini, and its transpacific ships now call at fewer ports and can make more round voyages.”

According to the analyst, Hapag-Lloyd achieved its “impressive” double-digit growth most notably in Asia-Europe, 15%, and on the transpacific and other Asia services, +8%.

Meanwhile, Cosco carried 13.3m teu in H1 25, which gave it a jump in lifted volumes of 7% year on year, adding more than 800,000 teu.

“Cosco’s mainland China business was again a major driver, bringing in an extra 250,000 teu of cargo year on year,” said Alphaliner.

Indeed, CEO of CTS Nigel Pusey told The Loadstar Podcast that Intra-Asia volumes, and carriers supporting those volumes, had benefited majorly from the trade war-driven rise in ‘China plus one’ strategies.

Listen to this clip of Nigel Pusey, CEO of Container Trade Statistics, speak about how alternative sourcing could be driving intra-Asia demand:

Alphaliner revealed that Yang Ming was the only of the top-10 carriers to report negative growth in the period at a “steep” 7.4% drop in lifted volumes, despite a slight increase in fleet capacity.

“It lost 7% of cargo on its ‘WE’, ‘PSW’ and ‘PNW’ services to the Americas, while volumes to the larger Middle East, South America, Red Sea, Australia, and South Asia region were down 15%,” the analyst explained.

At the same time, Maersk saw lifted volumes increase below market average at 2.2%, as did Evergreen at 1%, ONE at 1.5%, CMA CGM at 2% and ZIM at 2.3%.

Graph: Alphaliner

After the Q1 indication that Hapag-Lloyd could be in for a stellar year in terms of market growth, Mr Habben Jensen predicted that Q2 would also deliver similar growth levels and a “healthy volume development” but indicated uncertainty about Q3 and Q4.

“We’ll see quarters where there’s not going to be such stellar growth. I personally would expect that in the second half it’s going to be less growth than in the first half, but the real reliable indicators that we have for that are very few.”

Both Hapag-Lloyd and Cosco will be reporting Q3 liftings in their financial reports across the following weeks, along with the other major carriers, which will give further insight into the race for market share amid the growing trade war.

“Overall, carriers are likely to be pleased with such volume gains so far this year in light of the US tariff policy, although this and the new US port fees are expected to have a bigger impact on liftings in 2026,” summarised Alphaliner.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article