Container rate rally has more legs than bears assume

Precision needed on what drives box rates

WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISH

WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGSCHRW: HIGHER HIGHS ON THE RADARWTC: 'ONE RECORD'HLAG: EARNINGS GUIDANCE UPGRADE AAPL: GLOBAL SMARTPHONE SHIPMENTS VW: THE IMPACT VW: MASSIVE JOB CUTS CONFIRMEDEXPD: BULLISH

With spot rates on the Asia-Europe trades on a steady decline for the past three weeks and future demand increasingly uncertain, the prospect of significant overcapacity is rising.

“We have had no problems finding either space or equipment,” one Asia-Europe freight forwarder told The Loadstar last week, a clear anecdotal sign that demand is failing to keep step with supply.

And according to a new analysis from Sea-Intelligence Consulting, Asia-Europe carriers could well see vessel utilisation on the trade fall to loss-making levels in the coming months, unless capacity is adjusted.

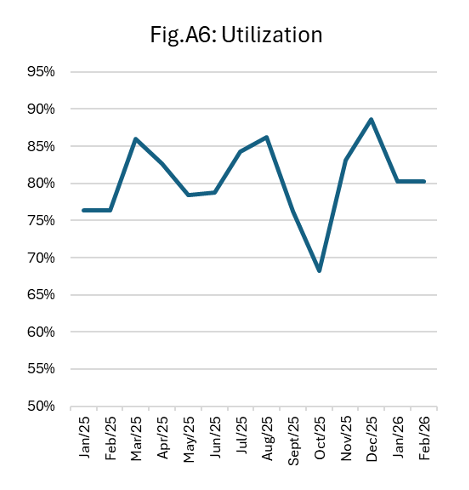

It noted that from early 2024, once it had become established that ships would no longer be able to transit the Red Sea and began routing via the Cape of Good Hope, vessel utilisation hovered at 82%-83%, apart from a “sharp decrease around Golden Week 2025, when a sharp drop (beyond seasonality) in demand was not matched by corresponding blank sailings”.

Source: Sea-Intelligence Consulting

Carriers’ reluctance to reduce capacity in October 2025 led to a corresponding decline in vessel utlisation in that month…

Source: Sea-Intelligence Consulting

… underscoring the direct links between demand and supply and utlisation.

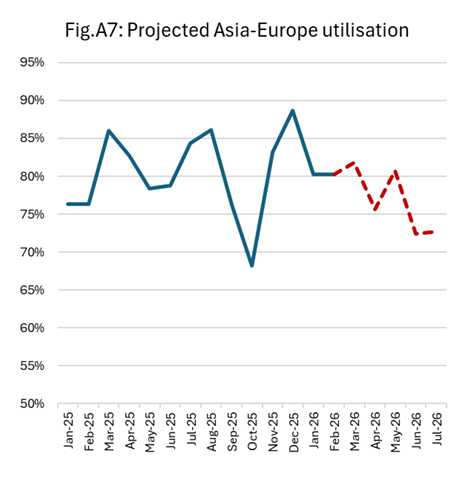

However, according to capacity projections from now until July, derived from carriers’ proforma schedules, even if the Asia-Europe trade continues to grow at the same strength as last year – Container Trade Statistics data shows 2025 ended with just over 19.8m teu transport from Asia to Europe, and showing 9.1% growth over 2024 – vessel utilisation is expected to drop this year.

Source: Sea-Intelligence Consulting

“We are on track for a weakening to the same level as seen in late 2022 and during 2023, a period where overcapacity became evident, and freight rates declined to loss-making rates for the carriers,” the analysts wrote.

“And please note that this is based on a strong 9.1% demand outlook for Asia-Europe in full-year 2026.

“If demand growth is below this, we are poised for a weaker situation than in 2023,” they added.

However, although CTS data for the first two months of 2026 ought to have encouraged carriers with strong early year trading – with February volumes up 45% on February 2025, although with the caveat of the different dates of Chinese New Year, Sea-Intelligence noted it was difficult to see how this could be maintained in the context of today’s economic shocks.

Source: Container Trades Statistics

“In all likelihood, we will see carriers pull some capacity from Asia-Europe, but it is likely this will be insufficient if demand also falters,” it added.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article