Battle for freighter capacity intensifies as airlines reshape networks

A cluster of shocks is forcing freighter operators to finely balance their global capacity – ...

VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTIONDHL: NEW HIGH TARGET ON THE STREET DSV: EXPECTATIONS RUN HIGH KNIN: DHL GUIDANCE UPGRADE READ-ACROSSKNIN: NEW OPENINGGM: TECH UPSIDEAMZN: BIG DEBT FUNDING ON ITS WAYDHL: 'STELLAR EXPRESS'DHL: UPDATEDHL: STRONG PRELIMINARY UPDATE CHRW: STILL VERY BEARISH

VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTIONDHL: NEW HIGH TARGET ON THE STREET DSV: EXPECTATIONS RUN HIGH KNIN: DHL GUIDANCE UPGRADE READ-ACROSSKNIN: NEW OPENINGGM: TECH UPSIDEAMZN: BIG DEBT FUNDING ON ITS WAYDHL: 'STELLAR EXPRESS'DHL: UPDATEDHL: STRONG PRELIMINARY UPDATE CHRW: STILL VERY BEARISH

News today shows that air cargo will enter 2026 with unexpected momentum, as peak-season volumes and rates rise across major tradelanes.

But carriers and brokers have warned that visibility beyond December is shrinking rapidly.

TAC Index data today shows rates climbing across most major Asia-origin corridors, with the global Baltic Air Freight Index up 6.5% in the week to 8 December, defying expectations of a constrained season.

Outbound Shanghai rose more than 7% week on week to exceed last year’s peak, while Hong Kong remained firm.

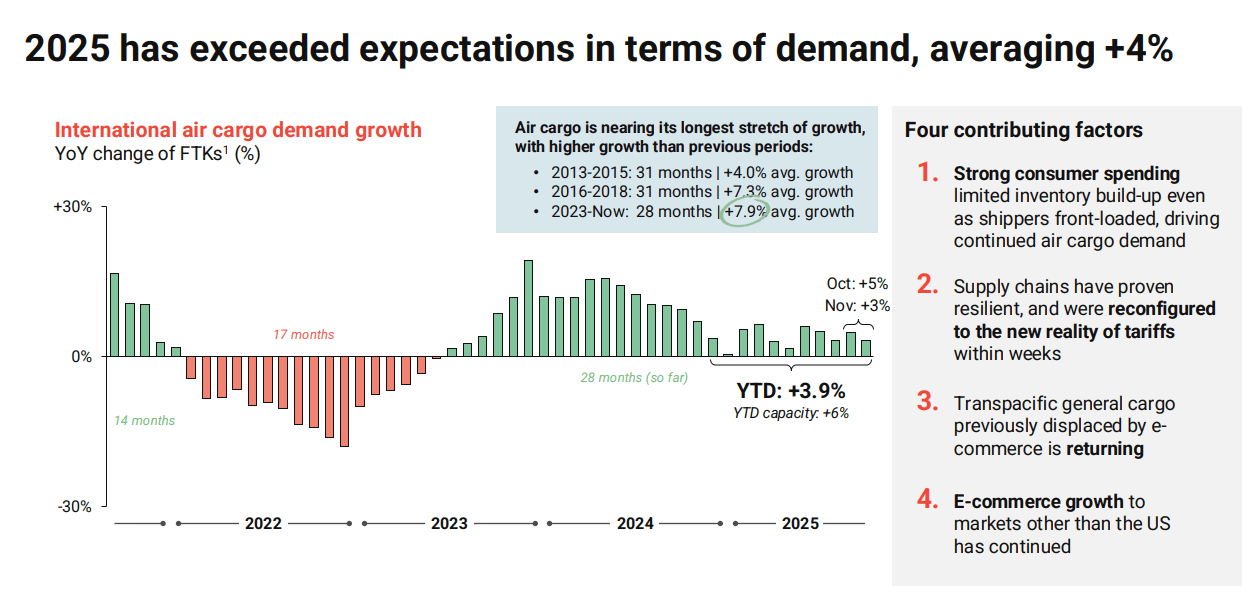

What has been surprising is not just the seasonal spike, but the resilience of underlying demand. According to Rotate, global air cargo is now in its 28th consecutive month of year-on-year growth, averaging 7.9%, outpacing previous multi-year expansion cycles.

Source: Rotate

Despite a softening ecommerce backdrop and shifting trade patterns, 2025 has still averaged nearly 4% demand growth, with October and November both recording positive gains.

This sustained growth underlines today’s note from Cathay Cargo director Dominic Perret, who said the season was “robust”, and “exceeding expectations”.

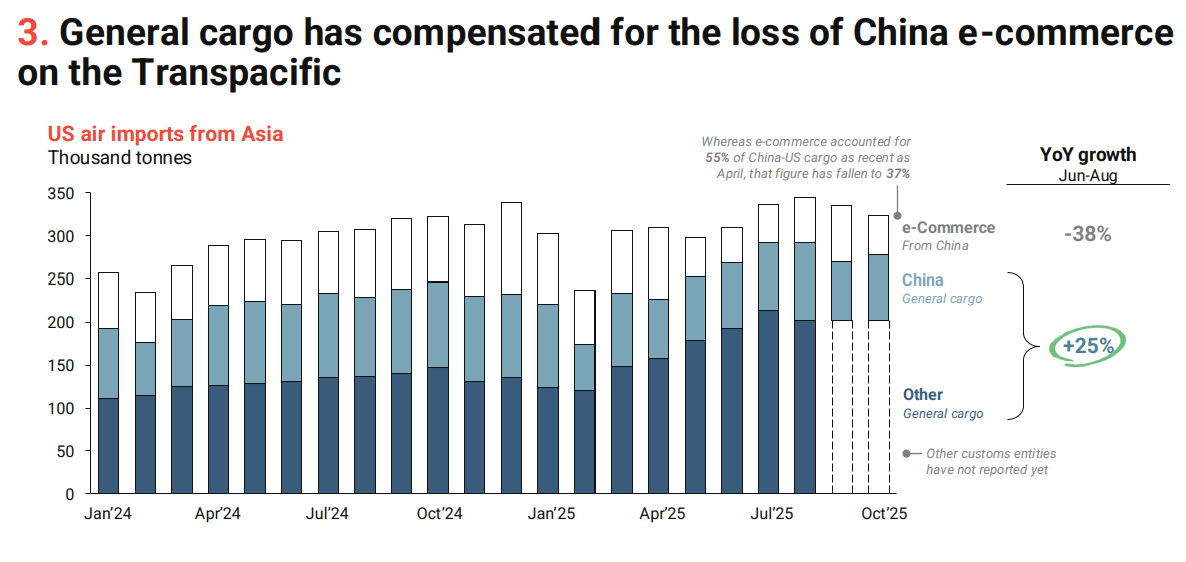

One of the more striking developments has been the rebalancing of the transpacific. China-US ecommerce volumes deteriorated sharply after peaking in early 2024, falling 38% between June and August, according to Rotate’s analysis of US import flows. Yet instead of collapsing, total Asia–US air imports remained stable, because general cargo rose 25% over the same period, effectively offsetting the decline.

Source: Rotate

This supports forwarder claims that some traditional cargo, displaced by ecommerce in 2023–24, is now returning, as rates and regulatory pressures normalise. It also shows why Asia–US lanes have remained unexpectedly strong during the peak: volumes have shifted in composition, but not gone.

Broker Chapman Freeborn said today that this illustrated an agile shipper base, capable of reconfiguring supply chains rapidly and reacting quickly to tariff and compliance changes.

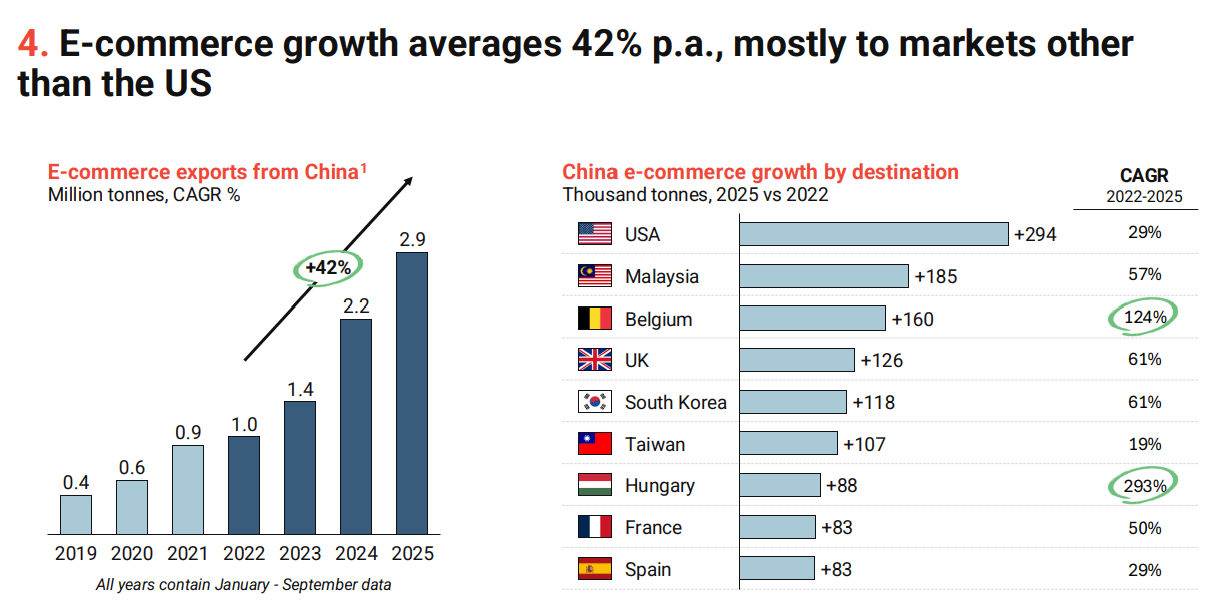

While the US remains the largest market by absolute volume, the charts reveal a new and important trend: China’s ecommerce growth is now overwhelmingly coming from non-US destinations.

Rotate data shows ecommerce exports from China rising at a 42% compound annual rate since 2019, with the biggest gains between 2022 and 2025 occurring in Malaysia, Belgium, the UK, South Korea, and Hungary.

Source: Rotate

This diversification underpins fierce competition emerging in Europe, noted by Cathay’s Mr Perret.

“As more and more ecommerce giants enter the European market, we have also added Madrid to our European cargo flight routes. We are well aware that the Asia-Pacific to Europe cargo market is extremely competitive, but the increased capacity reflects Cathay Pacific Cargo’s confidence in playing a significant role in this market.”

It also correlates with the aggressive expansion of Chinese freighter operators into Europe, which now account for most of the incremental capacity on the lane.

As Mr Perret explained, the imbalance between soaring imports and weaker export volumes in Europe has become a structural challenge, one Cathay is trying to solve by “aiming to load more high-yield cargo requiring careful handling on return flights to Asia”.

But despite the current buoyant volumes, the market remains uneasy.

Mr Perret asked: “The question is, what will the market look like in February?”

Demand is still softer than 2021–22 highs, and heavily reliant on volatile ecommerce segments. Chapman Freeborn described the environment as “tumultuous”, with more unknown variables, from tariffs to capital flows, than at any point since the pandemic.

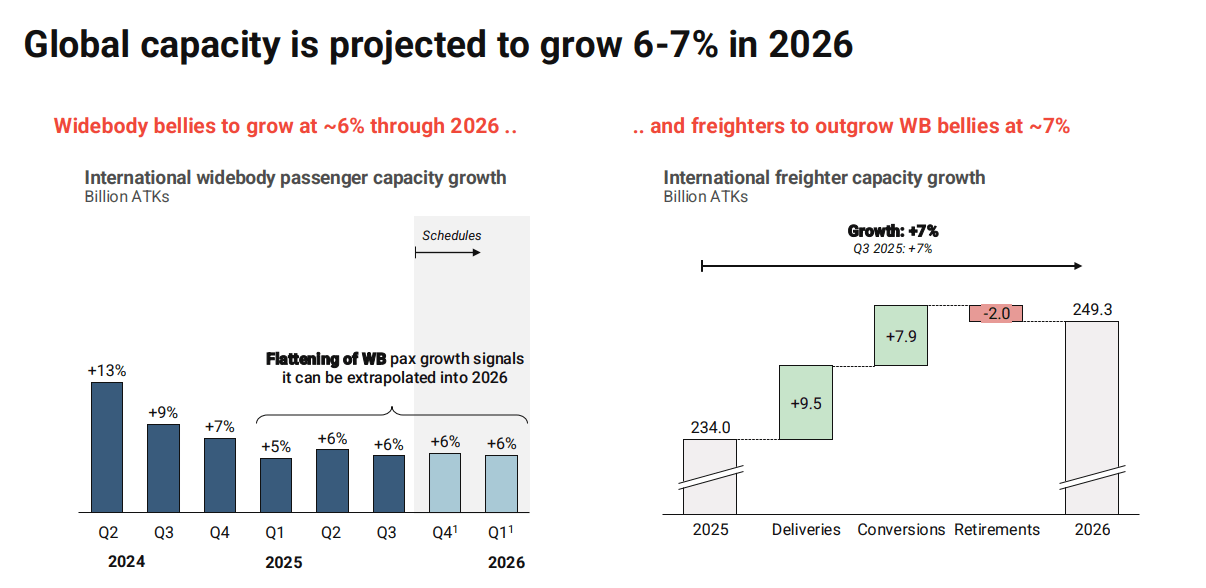

Meanwhile, Rotate’s data suggests global widebody belly capacity will expand around 6% next year, while freighter capacity will grow even faster, at 7%, supported by new deliveries and conversions, much of it driven by Chinese operators.

Source: Rotate

This raises a critical risk: if post-peak demand softens, the market could face rate pressure just as fresh capacity comes online, while the centre of gravity in freighter operations continues to move eastward.

For now, the season is ending on something of a largely unexpected high. But the combination of regulatory uncertainty, shifting consumer patterns, and more capacity ensures that the air cargo industry enters 2026 with both momentum and uncertainty.

The real story begins once this ‘mini’ peak ends.

This article is © The Loadstar. Reproduction, rewriting, or derivative use requires a license. Contact [email protected] for licensing enquiries.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article