US tariff on Brazilian exports looms amid array of new trade deals

The Trump administration will place a 25% tariff on certain Brazilian imports, marking the latest ...

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

Despite overcapacity seemingly to become a glaring issue in the liner industry, vessel idling still only represents a very small part of the global fleet.

Guillaume Caill, head of ocean EMEA at Flexport, said during yesterday’s freight market update: “There is indeed overcapacity looming in the long run on the ocean industry.

“New vessels are being built and will be delivered from now to 2030. The orderbook is around 30% of the total fleet on the water today – it’s massive.”

Mr Caill highlighted UNCTAD’s forecast of a comparative 12% global trade increase up to 2030.

“That’s between 2% and 3% in 2026, so it’s less than the capacity increase, which next year will be around 5% if the situation remains, and if Suez opens up and the situation returns to normal, then you’ll have an additional 7% capacity,” he warned.

“Carriers will, as usual, try to mitigate that via the different tools they have on hand,” he predicted, noting blank sailings, postponement of newbuild deliveries and scrapping.

“The rate of scrapping has been extremely low over the last five years since Covid,” he noted. “They might scrap a few more old vessels to get some capacity out of the market, but that’s going to be marginal compared to the newly built vesseld coming in.”

And Mr Caill warned that overcapacity would put pressure on rates.

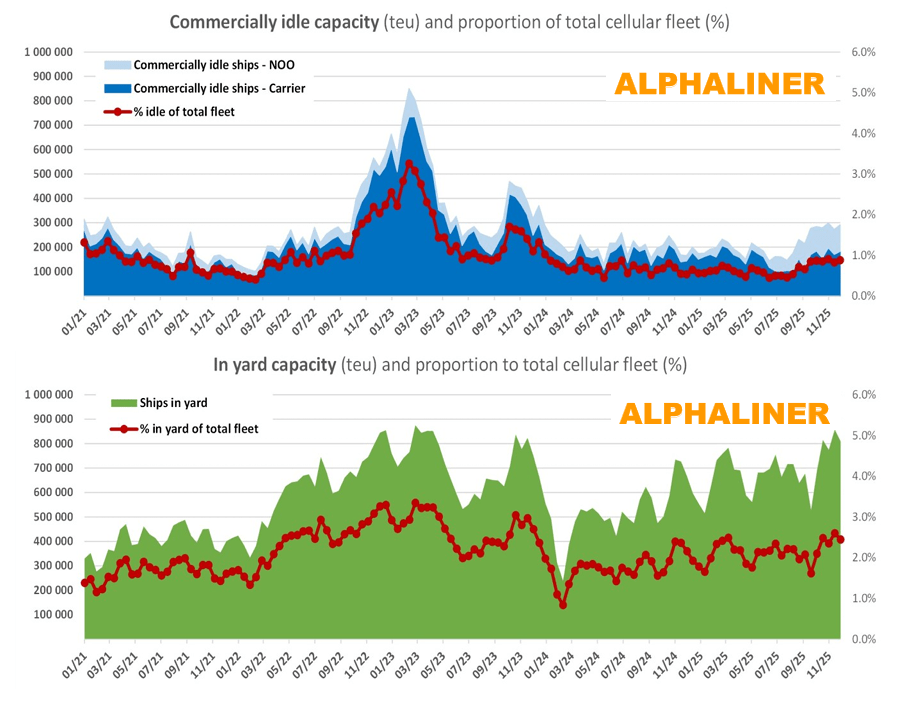

But despite this looming threat for carriers’ back pockets, commercially idle liner capacity has increased “only marginally” since September, according to Alphaliner, currently under 1% of global capacity, and “virtually unchanged” from a fortnight ago.

Idle vessels are defined as ships without revenue-generating activity – in warm or cold lay-up, between service assignments for longer than-normal, arrested, detained, abandoned, or idle for any other reasons.

As of 1 December, Alphaliner registered 0.9% of the world’s 33m teu fleet capacity as commercially idle. This equates to just 107 vessels with a capacity of 291,558 teu.

Graph: Alphaliner (click to expand)

Alphaliner reported that in the second half of the year, non-operating owners’ share of the idle fleet stood at just over 30%, and mainline carriers accounted for around two-thirds.

However, most were in the ‘vessels in limbo’ segment – containerships that have been detained, abandoned, under sanctions or in other legal problems – rather than any strategic moves to manage capacity.

“At the current level, commercial vessel idling remains a non-factor in the container shipping industry, but a slow start into 2026 and a traditionally weak first quarter could see vessel inactivity inch upwards,” concluded Alphaliner.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article