Inchape launches US forwarding service

Leading global port agency provider Inchcape Shipping Services is moving into the US freight forwarding ...

EXPD: QUOTE OF THE WEEKVW: MASSIVE JOB CUTSFDXF: FIRST TRADING UPDATE EXPD: MORE BULLISH THAN BEARISHFWRD: HUNTING FOR VALUEFDX: CAPITAL STRUCTURE ADJUSTMENTPLD: DOWN SHE GOESPLD: REIT DEAL-MAKINGFDX: HOLDING UPVW: BIG DIVESTMENTAMZN: AI INVESTMENTMAERSK: ANOTHER UPGRADE GXO: CONTRACT RENEWALFDX: SELL-SIDE REACTION TO INTERIMS

EXPD: QUOTE OF THE WEEKVW: MASSIVE JOB CUTSFDXF: FIRST TRADING UPDATE EXPD: MORE BULLISH THAN BEARISHFWRD: HUNTING FOR VALUEFDX: CAPITAL STRUCTURE ADJUSTMENTPLD: DOWN SHE GOESPLD: REIT DEAL-MAKINGFDX: HOLDING UPVW: BIG DIVESTMENTAMZN: AI INVESTMENTMAERSK: ANOTHER UPGRADE GXO: CONTRACT RENEWALFDX: SELL-SIDE REACTION TO INTERIMS

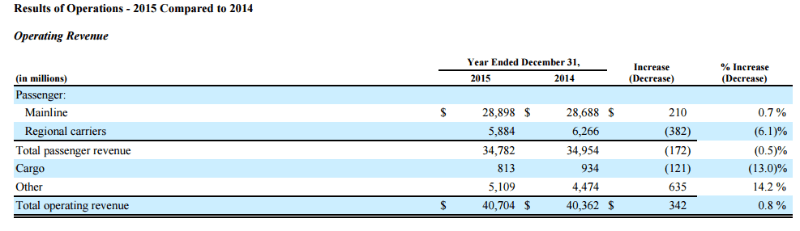

Cargo activities are under a huge amount of pressure at the “Big Three” US airlines. In case you missed the recent trading updates, United, Delta and American Airlines are all fighting business cyclicality in cargo just as their core passenger units are not faring particularly well.

So, what more appropriate juncture to run the rule on their cargo operations than at the end of a poor earnings season for most companies in the transport and logistics industry?

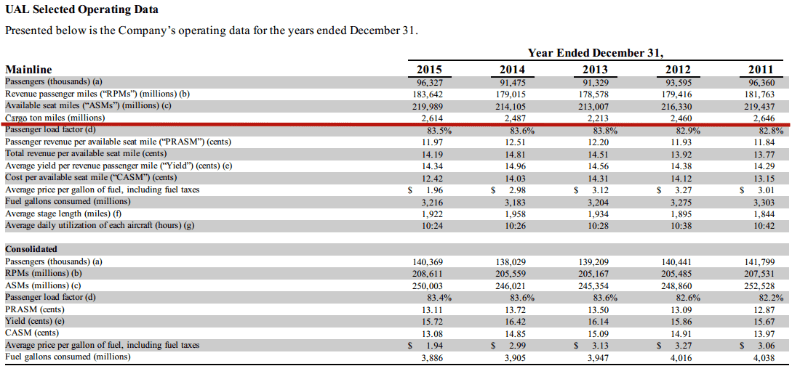

United

What a difference a year can make. In 2014, United saw cargo revenue increase by $56m, or 6.3%, over the year before, “primarily due to higher freight volumes and an improvement in mail revenue year-over-year, partially offset by lower yield on freight”.

Fast-forward to 2015, and what actually happened in terms of cargo cash flow and profitability in recent quarters is based upon our best guess, given that, aside from a few headline figures, United doesn’t give away too many financial details, either in its trading update nor in conference calls with analysts.

However, its cargo unit is shrinking, and trading conditions have deteriorated swiftly since the end of 2015.

United generated revenues of $937m in 2015, down 0.1% from $938m a year earlier, representing 2.4% of its total $37.9bn revenues. Cargo ton miles were essentially flat year-on-year, having risen 0.7% to 679m in the fourth quarter, and 5.1% to 2.6bn for the full year.

In the fourth quarter, cargo sales dropped 11.2% to $231m, which compares with a 19.8% plunge in the three months ended 31 March, when its revenue declined to $194m from $242m year-on-year. Cargo revenue totalled 2.3% of its $8.2bn quarterly sales at group level.

During the first quarter, cargo ton miles dropped 6% to 622m, year-on-year. Notably, not once was cargo mentioned in the conference call that followed its quarterly trading update release on 21 April.

Since the turn of the year, United shares have fallen 18%, and management acknowledges that the carrier’s operational performance has not been particularly good, reflected in the depressed trading multiples of its shares.

The chart below shows the development of United’s operations since 2011.

Sources: United Airlines

If anything, cargo activities appear to be a distraction, and I wonder why United retains any exposure at all to cargo if it doesn’t plan a response to the more difficult environment characterised by soft demand.

The same applies to its main rivals, Delta and American Airlines, which are waiting in the wings and seem to have no intention of entertaining a more aggressive corporate strategy.

Delta

Cargo revenue at Delta fell dramatically in the first quarter of 2016 – down 25.3% to $162m, from $217m, year-on-year, primarily due to weaker international demand.

Cargo sales amounted to 1.7% of Delta’s total $9.2bn first-quarter revenues, which were down 1% year-on-year. Its recent cargo performance is worse than United’s: in the fourth quarter last year, cargo revenue plummeted 21% to $193m; and by 13% to $813m for the full year.

Source: Delta Airlines

As with United, cargo operations didn’t receive a single mention in the call that followed Delta’s quarterly results release, while its share price is down 14% so far this year. Its stock currently trades at a premium to United’s, which seems justified by a higher forward yield.

In other news, Delta said on 29 April it had “reached aa deal with Airbus worth over $4bn to acquire 37 additional A321s as part of its efforts to renew its narrowbody fleet. “The fuel-efficient A321s will replace older-generation jets, including the MD-88,” it said.

American

The financials of American Airlines show annual cargo revenue decreased $115m in 2015, down 13.1% to $760m year-on-year, due to falling freight yields. Cargo sales amounted to 1.8% of the carrier’s total revenues of almost $41bn last year.

It opened a new 25,000sq ft dedicated pharmaceutical cargo cold storage facility in Philadelphia in the final quarter of 2015, but also experienced a 17.3% fall in cargo revenues to $192m for the period, with cargo ton miles falling 2.1% to 598m and cargo yield per ton mile down 15.5% to 32.07 cents.

Recent trends are not particularly encouraging, either. In the three months ended 31 March, cargo revenue fell 16.8% to $162m, due to declining freight yields both domestically and internationally. Cargo ton miles for the quarter were down 1.8% to 543m, while cargo yields per ton mile dropped 15.3% to 29.77 cents from 35.1 cents.

American’s shares are down 15% this year, but at least cargo merited a mention in the recent call with analysts!

Last summer, I wrote about the cargo activities of the “Big Three“, arguing that the devil was in the detail, and cargo strategy “would gauge their ability to cover multiple aspects of their global businesses, while maintaining financial discipline”.

I noted about a year ago: “It will also say a lot about their broader strategy – in this context, all three carriers are at a very critical juncture.”

Their shares are falling at a time when little attention is paid to smaller assets that could provide some relief, particularly if more capital was devoted to expand their footprint inorganically. In my view, if things do not change rapidly, we could soon hear about divestments or cost-cutting measures, rather than new investments in those units.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article

David Hoppin

May 03, 2016 at 2:17 pmBig Three US carriers have only belly cargo exposure, primarily international. Hard to imagine many long-haul widebody flights would be LESS profitable overall if they did not carry cargo, even at current depressed yields. So makes no sense to quit carrying cargo. What to do? Hard to see how vertical integration (i.e., adding door-to-airport/door-to-door service in most markets) would be profitable for any pure belly carrier. Therefore only strategic option seems to be horizontal integration of some kind — i.e. each of the Big Three U.S. carriers combining their respective cargo businesses with those of other airlines in order to drive some cost savings but mainly revenue benefits due to stronger network that is more important to customers (forwarders). Obviously competition authorities will have a say, but most A2A cargo markets are significantly less concentrated than corresponding passenger markets so not sure regulators will block cargo consolidation.

Ale Pasetti

May 04, 2016 at 6:59 amDavid,

Thanks much for your comment.

Double or quits cargo? This is a very hard call, given that we do not not know the level of required return and investment there. So, at present I might disagree with your view at least until we are blind on financials (“Hard to imagine many long-haul widebody flights would be LESS profitable overall if they did not carry cargo, even at current depressed yields.”).

Do you happen to know their current level of profitability and invested capital?

But I agree with your view on vertical integration, and your take on consolidation makes a lot sense.

Best,

Ale

Tim Strauss

May 08, 2016 at 11:07 pmEasier to discuss off line if interested in the financials.

Ale Pasetti

May 12, 2016 at 4:49 amFeel free to get in touch at [email protected]. Would be great to talk about it. Thanks, Tim.