Network restructuring cascading larger vessels onto Intra-Europe trades

Container lines are increasingly deploying larger vessels on intra-Europe routes, with the number of ships ...

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

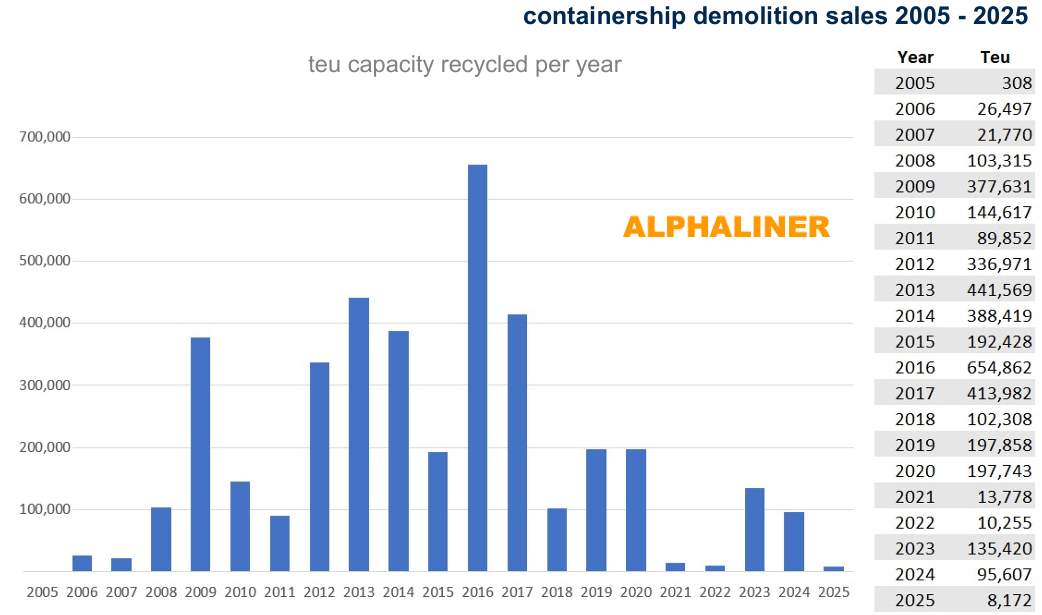

The global container shipping industry all but avoided the recycling market last year, vessel scrapping falling to its lowest level in two decades as strong freight demand and robust charter rates kept even the oldest ships trading.

According to new data from maritime analyst Alphaliner, just 12 box ships were scrapped during the year, representing a combined capacity of 8,172 teu – a further three, smaller units, sold for recycling had still to be demolished by year-end.

The total was dramatically below the already subdued 2024 figure of 95,607 teu, and a fraction of the 655,000 teu scrapped at the recycle peak in 2016.

Source: Alphaliner

Owners instead opted to maximise earnings in a lucrative trading environment, according to Alphaliner.

“The healthy container shipping market, with high demand for tonnage and robust charter rates throughout the year, largely explains shipowners’ reluctance to dispose of older vessels,” it said.

The limited demolition activity was concentrated almost entirely in the smaller vessel segment. Ten of the 12 ships scrapped were below 1,000 teu, underlining how even modest tonnage retained employment in a market stretched by long-haul routings and capacity absorption.

The largest vessel sent for recycling was the 2,407 teu Horizon Enterprise, built in the US in 1980, the smallest was the 286 teu Zi Yu Lan, a rare German-built vessel capable of carrying nearly 400 passengers alongside its cargo.

Overall, the average age of ships scrapped in 2025 was 30 years, the oldest was 45 and the youngest 20, highlighting how far owners are willing to push vessel lifespans when market conditions allow.

But despite the weak market, demolition prices remained historically firm. Prices in the Indian Subcontinent softened slightly during the year, but stood at $400-$430 per light displacement tonne (ldt) in December. Prices in Turkey also declined early in the year before stabilising at $270-$290 per ldt.

Source: Alphaliner

Looking ahead, Alphaliner said, the trajectory of scrapping hinged on one critical variable – a return to Suez and Red Sea transits – as a widespread end of Cape of Good Hope diversions would sharply reduce tonne-mile demand, releasing capacity back into the market and triggering vessel cascading.

“Freight and charter rates could come under significant pressure, leading shipowners to consider scrapping some of their older tonnage,” Alphaliner said, forecasting a potential rebound in recycling sales in the second half of 2026.

However, that scenario remained uncertain, it added, amid the instability in the Middle East and renewed security threats in the Red Sea.

Should Cape diversions persist this year, Alphaliner forecasts that trading conditions could remain strong enough for owners to largely avoid recycling again, deferring a scrapping surge to 2027 and 2028 when a wave of newbuild deliveries is expected to force fleet rationalisation.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article