A new era for shippers, with blanked sailings now a fact of life

Container shipping has entered a new era of structurally constrained capacity, as carriers routinely withdraw ...

PLD: PROPOSAL DETAILSPLD: FINAL OFFERDSV: ROAD CEO MATTERSDSV: VOLUME PROGRESSION IN SEA FREIGHT DSV: TIME TO INCREASE THE VOLUMES IN SEA FREIGHTDSV: HEADCOUNT DISCREPANCIESDSV: TRASHEDDSV: IT IS A MATTER OF TRUSTDSV: FREE CASH FLOW QUESTIONEDDSV: QUESTION TIMEDSV: CEO ON SCHENKER INTEGRATIONDSV: CFO PREPARED REMARKSDSV: CEO PREPARED REMARKSDSV: CONF CALL FWRD: SHOOTING UPKNX: TRADING UPDATE ON THE WAY GM: TRADING UPDATE OUTUPS: REMEMBER THE TAILWINDS

PLD: PROPOSAL DETAILSPLD: FINAL OFFERDSV: ROAD CEO MATTERSDSV: VOLUME PROGRESSION IN SEA FREIGHT DSV: TIME TO INCREASE THE VOLUMES IN SEA FREIGHTDSV: HEADCOUNT DISCREPANCIESDSV: TRASHEDDSV: IT IS A MATTER OF TRUSTDSV: FREE CASH FLOW QUESTIONEDDSV: QUESTION TIMEDSV: CEO ON SCHENKER INTEGRATIONDSV: CFO PREPARED REMARKSDSV: CEO PREPARED REMARKSDSV: CONF CALL FWRD: SHOOTING UPKNX: TRADING UPDATE ON THE WAY GM: TRADING UPDATE OUTUPS: REMEMBER THE TAILWINDS

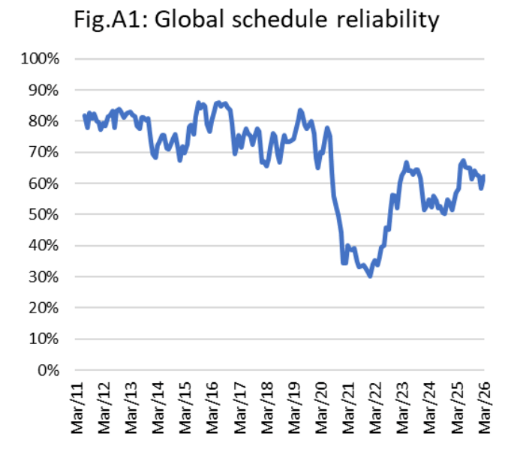

Container shipping is settling into a “new normal” of lower schedule reliability, with knock-on effects that continue to absorb global capacity, according to the latest analysis from Sea-Intelligence.

New data covering March shows that, despite incremental improvements by some carriers, overall reliability has still not returned to pre-pandemic levels.

Instead, the industry appears to have stabilised at a markedly weaker baseline.

Analysts at Sea-Intelligence explained that, between 2011 and 2019, schedule reliability ranged between 70% and 80% – in the current environment, performance has plateaued between 50% and 65%.

“It is becoming evident that despite efforts, and success from some carriers, to improve schedule reliability, we are not seeing a reversal to pre-pandemic normality,” one analyst said.

Source: Sea-Intelligence

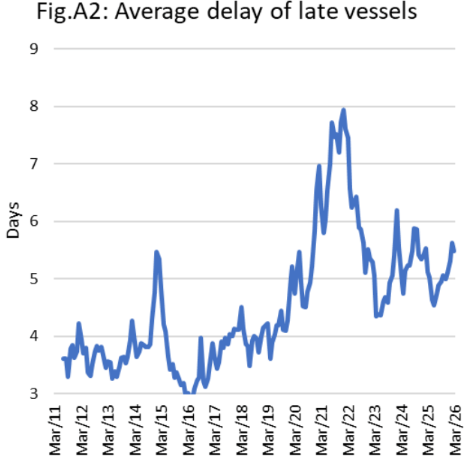

At the same time, the severity of delays has worsened. Pre-pandemic, vessels were typically delayed three to four days; now, average this is 4.5 to 5.5 days, further compounding the operational impact.

Source: Sea-Intelligence

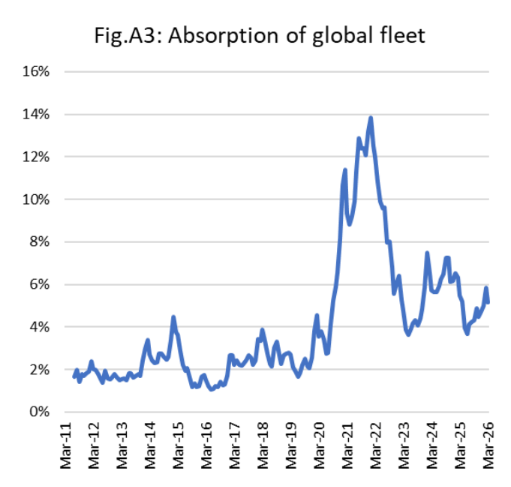

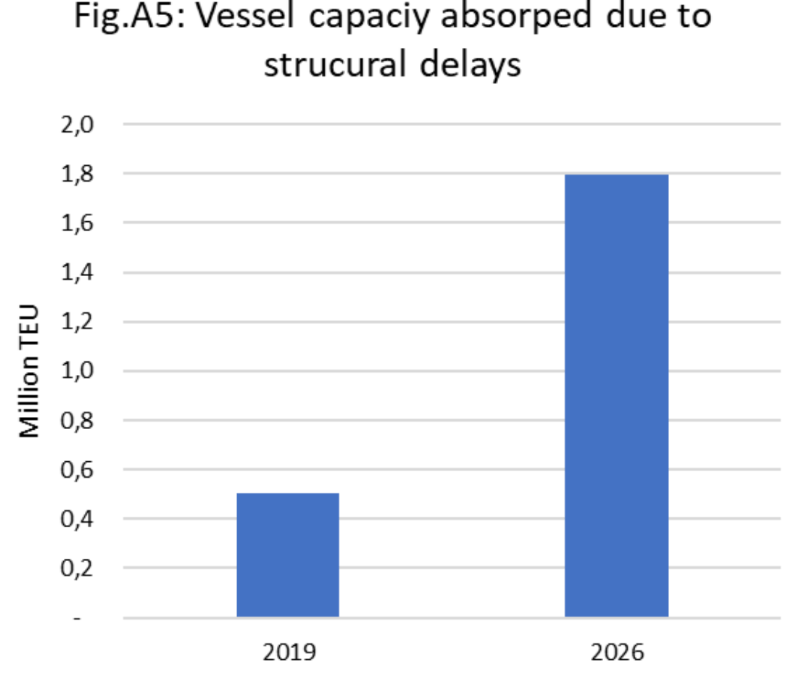

Sea-Intelligence noted that the percentage of late vessels, combined with the duration of delays, could be used to calculate the capacity effectively absorbed by the delays and, hence, unavailable to the market.

“This seeming structural shift to a large risk of delays, as well as longer delays, will inexorably lead to a larger share of global capacity being absorbed,” the analyst warned.

Historically, around 2.2% of global capacity was absorbed in this way, described as a relatively stable baseline that underpinned supply-demand dynamics.

Source: Sea-Intelligence

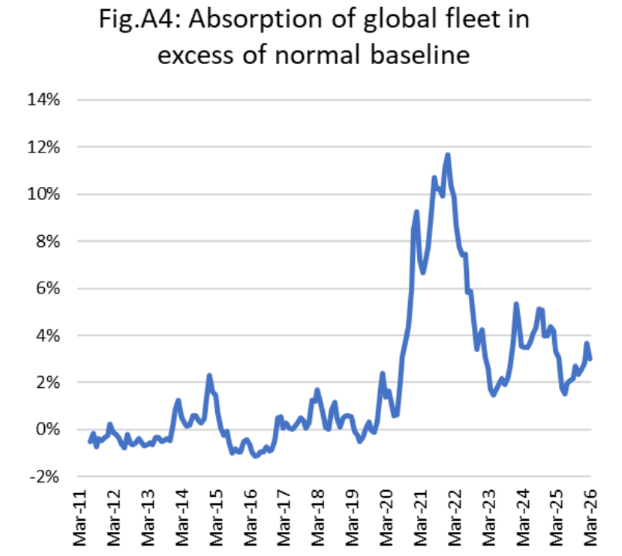

However, against this historical baseline, deviation now consistently sits between 2% and 4% above normal, with no clear signs of improvement.

Source: Sea-Intelligence

As a result, the share of capacity absorbed by delays has effectively doubled, or even tripled, and ranges between 4% and 6%. The average for the period between 2023–2026 is 5.3% – In nominal terms, a substantial impact.

Based on current fleet sizes, Sea-Intelligence estimates that approximately 1.8m teu of capacity is effectively “missing” from the market, due to schedule delays – equivalent to a fleet almost the size of that of the world’s seventh-largest liner, Evergreen.

Even when isolating only the increase above pre-pandemic norms, the effect remains significant.

The additional 3.1% of absorbed capacity translates to around 1.06m teu, comparable with removing a top-10 carrier such as HMM from global operations.

Source: Sea-Intelligence

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article