Battle for freighter capacity intensifies as airlines reshape networks

A cluster of shocks is forcing freighter operators to finely balance their global capacity – ...

GM: TRADING UPDATE OUTUPS: REMEMBER THE TAILWINDS PLD: NEW RELEASEPLD: OUCHVW: NEW PARTNERS SOUGHTEXPD: AIRCRAFT ON GROUND SERVICESTSLA: JUST AS VW STRUGGLESBA: NEW BIG ORDERBA: THE ORDERBOOK GROWSPLD: PUSHING FOR A DEAL PLD: TIME TO DEALEXPD: ANOTHER ALL-TIME HIGH CHRW: NEW RECORD DSV: AHEAD OF EARNINGS RELEASE JBHT: NEW HIGHS EVERYWHERE

GM: TRADING UPDATE OUTUPS: REMEMBER THE TAILWINDS PLD: NEW RELEASEPLD: OUCHVW: NEW PARTNERS SOUGHTEXPD: AIRCRAFT ON GROUND SERVICESTSLA: JUST AS VW STRUGGLESBA: NEW BIG ORDERBA: THE ORDERBOOK GROWSPLD: PUSHING FOR A DEAL PLD: TIME TO DEALEXPD: ANOTHER ALL-TIME HIGH CHRW: NEW RECORD DSV: AHEAD OF EARNINGS RELEASE JBHT: NEW HIGHS EVERYWHERE

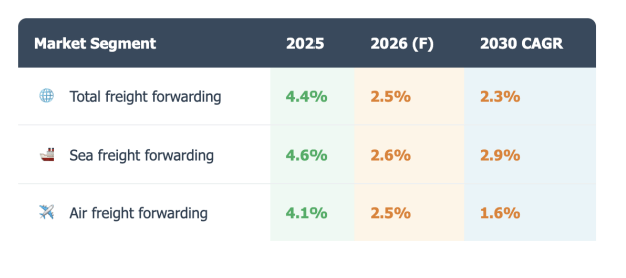

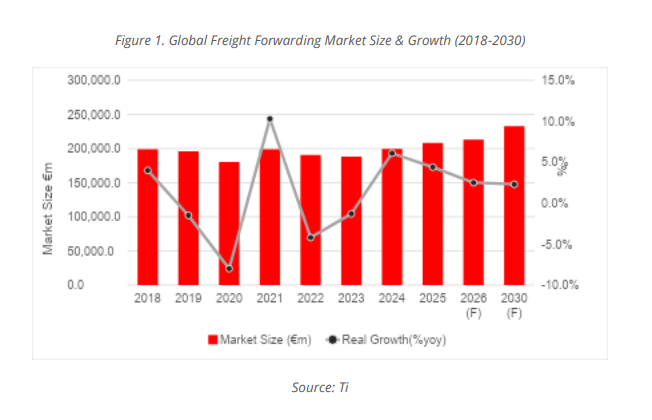

The global freight forwarding market is still growing, but the industry’s easy gains appear to be over as slowing trade growth, geopolitical disruption, and persistent overcapacity squeeze margins.

According to Transport Intelligence’s latest Global Freight Forwarding Market Size & Forecast report, the market grew 4.4% in real terms in 2025, reaching €208.1bn ($240bn). However, growth is expected to slow sharply this year, the market forecast to expand by just 2.5%.

Both air and sea forwarding are expected to see weaker growth. Air freight forwarding, which grew 4.1% in 2025, is forecast to increase just 2.5% this year, while sea freight forwarding growth is expected to slow from 4.6% to 2.6%.

Source: Ti

The slowdown comes amid a more challenging operating environment. Ti points to weaker trade growth, ongoing disruption in the Middle East, and structural overcapacity in ocean freight, all of which are making it harder for forwarders to translate volume growth into profits.

That pressure appears to be spilling into relationships with shippers.

At TIACA’s Air Cargo Forum in Warsaw last week, Mark Chadwick, president of the Global Shippers Association, told The Loadstar some forwarders had sought substantial surcharge increases following recent market disruption, with requests varying wildly between providers.

The association attempted to establish a common framework for surcharge support across its forwarding partners, but abandoned the exercise after receiving requests ranging from no increase at all to as much as 250% on the same tradelanes.

“A couple were trying to make the year on a couple of months,” he said, adding that some members felt they were being “completely taken advantage of”.

While Mr Chadwick acknowledged that disruption had created genuine cost pressures, he suggested some forwarders had been more aggressive than carriers in seeking additional compensation. He also noted that demand remained weak and capacity plentiful in several markets, limiting carriers’ ability to push through sustained rate increases.

Indeed forwarders have told The Loadstar their margins are severely under pressure.

Yet despite slowing growth and the growing pressure on profitability, investors continue to see opportunity in logistics.

According to the latest Global Logistics M&A Recap Report, from Ti and Logisyn Advisors, Europe accounted for 54.2% of all logistics acquisitions in May, with North America accounting for 25%.

Last-mile operators were the most popular acquisition targets, followed by software providers. However, many of the most significant deals reflected a growing interest in specialist logistics capabilities, including customs brokerage, project logistics, and ecommerce fulfilment.

Among these were fulfilmentcrowd’s acquisition of Dutch ecommerce specialist Fulfilment.nl; Ceva Logistics’ purchase of heavy-haul specialist Fagioli Group; and Redwood Logistics’ acquisition of customs broker EELCO.

Mikael Olesen, MD of Logisyn Advisors, said customs expertise had become increasingly valuable as tariff changes and trade complexity reshaped supply chains.

“Buyers are acquiring customs capability not just for revenue, but as a differentiator,” he said.

Scale alone no longer appears to be enough for the forwarding market. The winners are increasingly likely to be those able to offer services customers cannot easily source elsewhere.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article