Cautious air cargo shippers delay tenders amid signs rates may have peaked

Air cargo shippers are increasingly delaying tender decisions and extending existing contracts, rather than locking ...

DSV: STOCK MARKET REACTION XOM: OIL INVENTORY WARNINGWTC: EBL DEAL DETAILSWTC: EBL DEALEXPD: 'READ MY LIPS' HON: DEALS ON THE MENUEXPD: NEW RECORD XPO: THE REBOUNDCAT: PAYOUT UPDHL: LIGHTHOUSEMAERSK: ANOTHER UPGRADEFWRD: HEALTHY CORRECTION R: RYDER CEO SAYS

DSV: STOCK MARKET REACTION XOM: OIL INVENTORY WARNINGWTC: EBL DEAL DETAILSWTC: EBL DEALEXPD: 'READ MY LIPS' HON: DEALS ON THE MENUEXPD: NEW RECORD XPO: THE REBOUNDCAT: PAYOUT UPDHL: LIGHTHOUSEMAERSK: ANOTHER UPGRADEFWRD: HEALTHY CORRECTION R: RYDER CEO SAYS

Air freight markets are unlikely to normalise any time soon, despite the US-Iran ceasefire, with analysts warning the industry has entered a more volatile, supply-constrained phase.

Speaking on next week’s The Loadstar News in Brief Podcast, Maarten Wormer, head of consulting at Aevean, said the disruption had already significantly dented expected growth.

“We’ve effectively lost around six percentage points of expected weekly air freight growth globally,” he said. “At the start of the year we were expecting 5–6% growth, but we’ve already lost around one percentage point of that.”

While the ceasefire may ease immediate pressure, he warned recovery would take far longer.

“Normalisation is still very, very far away… fuel is one of the big drivers,” he said, noting tanker shipments to Europe could take up to 40 days.

“In Asia, jet fuel prices are around 160% higher than last year… that will take way more than the two-week ceasefire to normalise.”

Recent data suggests the market has already shifted into a new phase.

According to Cargo Facts Consulting, March marked an “inflection point” where capacity constraints, fuel costs, and geopolitical risk overtook seasonality as the primary drivers of pricing and network behaviour.

TAC Index data shows the Baltic Air Freight Index rose more than 25% over the four weeks to early April, pushing rates back towards peak season levels, with far steeper increases on key lanes.

Spot rates from Hong Kong to Europe climbed sharply through March, while rates from India to Europe more than doubled, reflecting tightening supply rather than stronger demand.

Source: Rotate

Capacity data from Rotate illustrates how abruptly the market has shifted. Year-on-year growth spiked earlier in the year before falling sharply into negative territory as the impact of Middle East disruption took hold, signalling a move from expansion into instability.

“Normally we would route everything via the Middle East,” one freight trader told TAC Index. “Now there is less flexibility, transit is longer and costs are much higher.”

Source: Rotate

But while disruption has been severe, global capacity has not collapsed.

Rotate data shows freighter capacity rose 9% month on month in March, but with sharp regional divergence. Routes touching the Middle East saw double-digit declines, while Asia–Europe and transpacific lanes posted strong gains.

This reflects a rapid reconfiguration of global networks, with airlines shifting capacity towards corridors offering greater operational certainty and pricing power.

At the height of the disruption, as much as 15–20% of global capacity was estimated to be offline. Although some has since returned, longer routings and operational inefficiencies mean effective capacity remains significantly tighter than nominal supply.

Source: Rotate

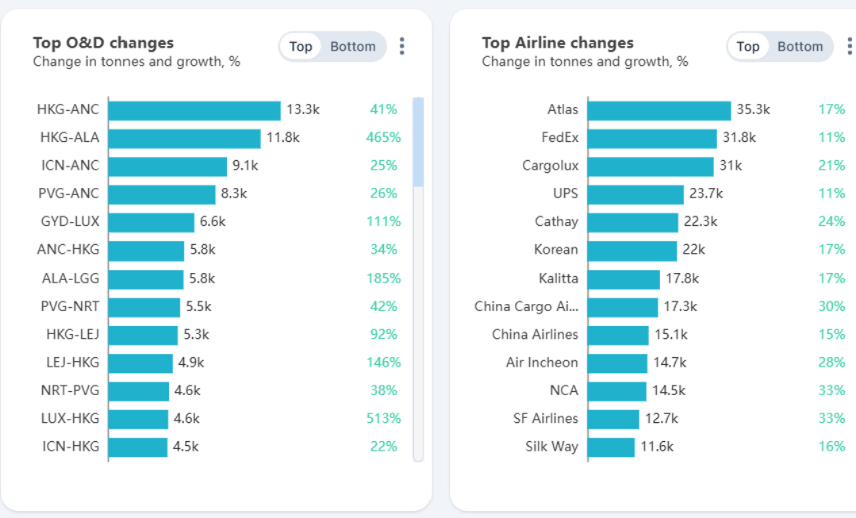

As networks reconfigure, Asia–Europe has emerged as the key beneficiary. With Gulf hubs constrained, airlines have shifted towards more direct routings and alternative hubs. Cargo is also being pushed through secondary hubs, with strong growth on lanes via Anchorage and Central Asia, highlighting how networks are adapting to bypass disrupted regions.

By contrast, Asia–North America lanes have weakened, reflecting both softer demand and continued policy uncertainty.

Source: Rotate – capacity changes March 2026 vs February 2026

The disruption has also shifted the balance between freighter and passenger capacity. Freighter operators including Atlas Air, FedEx, and Cargolux have increased capacity, helping to offset lost Middle Eastern bellyhold lift. At the same time, cargo flows have become more fragmented, with performance varying sharply by region, hub and commodity type.

The surge in rates is being driven less by demand, and more by cost inflation and shorter supply.

Jet fuel prices have risen dramatically, in some cases more than doubling over the past month, driven by both crude price increases and widening refining margins, which has had a disproportionate impact on lower-value cargo.

Mr Wormer said perishables were particularly exposed due to their low value density, while ecommerce shipments could also come under pressure as margins tighten. By contrast, high-value cargo such as data centre equipment is expected to remain resilient.

Despite signs of recovery, volatility is expected to remain the defining feature of the market in the near term. Even if conditions stabilise, rebuilding networks, restoring confidence and rebalancing fuel supply chains will take time.

As Cargo Facts notes, air cargo is no longer moving in a synchronised way, but is becoming “a fragmented system shaped by capacity reallocation and external shocks”.

Check out this week’s The Loadstar Snapshot, on why air cargo fuel surcharges are splitting apart…

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article