BAL re-enters liner trades with transpacific loader

Opportunistic Chinese shipowner BAL Container Line is making a selective comeback to the transpacific trade, ...

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

PLD: TRADING UPDATE ON THE WAY KNIN: UPSIDEJBHT: STRONG TRADING UPDATE DSV: EVERY LITTLE HELPSJBHT: CEO REMARKS WMT: VERTICAL INTEGRATION IN LOGISTICSJBHT: HERE WE GOPG: STEADYEXPD: NEW RECORD BA: DELIVERIESMAERSK: BEAR CAMP MUSINGS

Containership time-charter markets have, with few exceptions, experienced a rollercoaster ride since the start of 2020.

After a generally weak start to the year for feeder vessels and a continuation of 2019’s strong markets for mid-size and larger units, the onset of lockdowns drove a correction in vessel earnings.

Since then, however, time-charter markets have roared back into life, and vessel earnings for key benchmarks have risen at least as fast, if not faster than they fell earlier in the year.

Starting with where the recovery has been strongest, among midsize and larger assets, there are several clear drivers of the strong markets seen over the past month.

What has driven the performance of these assets is also of relevance across the vessel size spectrum, since there seems to be a clear ‘trickle-down’ effect in which liner companies unable to hire units in ‘sold out’ segments of the market have instead fixed the largest available option.

Since the start of Q3, the number of 4,000 teu-plus vessels available for hire has shrunk at an incredibly fast pace. For 4,000-5,000 teu assets in particular, the potential backlog of idle units to work through – more than 50 at the peak of the crisis – meant that a sluggish recovery was a sensible assumption (for 5,000 teu-plus assets markets are less liquid in general, and as we have noted over a number of years what makes the difference between a weak, mediocre and strong market can be a single-digit shift in the number of available units).

Looking at the data, the recent clear-out of available units was driven by three factors.

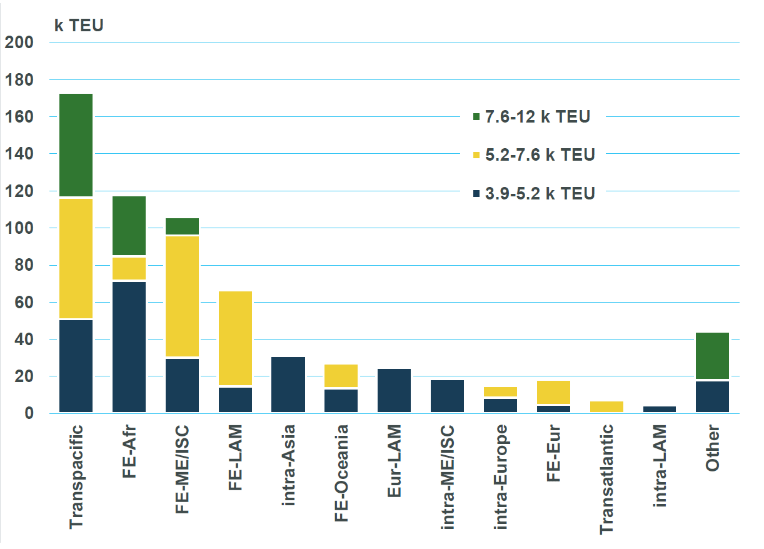

As the chart above reveals, the stand-out source of new deployment for mid-size vessels is the transpacific trade, where around 170,000 teu of midsize tonnage was sent after being fixed since the start of July. This of course partly reflects the fact that the transpacific is a major source of deployment for vessels of this size in normal times.

But in this instance the moves by liner companies to reinstate capacity as quickly as possible and offer extra sailings led to a sweep of the market for mid-size units. Liner companies were clearly incentivised to capitalise on high spot freight rates as much possible during the recent transpacific import surge, and this required fixing vessels at short notice.

This dynamic coincided with a number of new service launches and reorganisations on the Asia-West Africa trade, most notably CMA CGM’s ‘Round The Africa’ service that uses 11 ‘classic’ panamaxes in a service that transits Suez on the headhaul voyage and the Cape of Good Hope on the return leg. Not having sufficient appropriately sized vessels to spare, the charter market provided the balance. CMA CGM’s launch also coincided with Africa-related fixing by other global liner companies.

Finally, at least before timecharter rates began to really climb, a number of regional operators headquartered in the Middle East and Indian subcontinent region picked up smaller post-panamax units for deployment on intra-regional routes. This has been an increasing practice over the past five years, and one that has picked up steam over the past 18 months in particular (likely since once one liner moves to upside its assets others are pressed to match their more favourable slot cost economics).

In combination, these three factors caused a sudden rush into the market, where demand for panamaxes in particular was driven by both charterers who wanted assets of that size and those who had been locked out of the market for larger units.

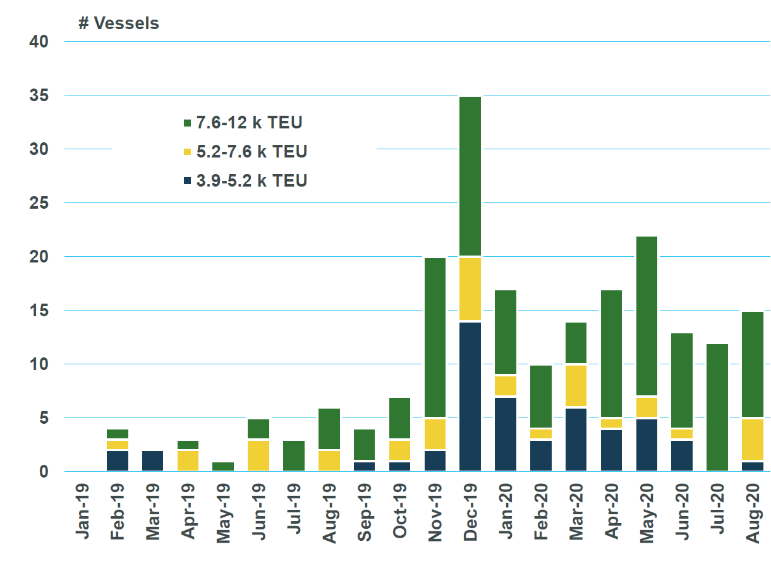

That concerns demand for mid-size units – there are also supply-side developments to consider. This does not so much concern the current situation, where there simply is very little, if anything, available to hire and few larger units likely to become available in the near-term. When the number of available units is really whittled down, an elastic upward timecharter rate response is what nearly always takes place. Rather, what is perhaps underappreciated is that the number of available mid-size units has been restricted this year by scrubber retrofitting activity.

The chart above shows the number of midsize containerships by month of scrubber retrofit completion since the start of 2019. Scrubbers, of course, have been key to the fortunes of this size of asset for over a year now, but what is different this year is that it is largely midsize vessels undergoing retrofits themselves – rather than filling the rotations of larger vessels temporarily out of action – that has restricted the supply of available units.

So what happens next, and how far down the vessel size spectrum will the recovery reach? In the very near-term the outlook is healthy: for 5,000 teu-plus units in particular there is likely to be a very limited pipeline of units coming available for hire, and as a result there will be few mechanisms to cause a rise in the economically idle fleet. If the challenge for sub-1,500 teu feeders over the past several years has been a chronic overhang of idle units that effectively ‘handicaps’ the market, even if fixtures activity is healthy, 3,000 teu-plus units for the time being face largely the opposite situation.

Once we move into the fourth quarter of this year, we expect that the market rally for larger units will run out of steam and rates will see a fairly modest correction. We expect that the latter part of the year will be more challenging from a demand-side perspective for liner companies (although this is by no means certain), and that an initial move to reverse lockdown-era network restrictions akin to a retailer restocking inventory will give way to a more gradual need to add capacity. Units chartered for short durations during the transpacific import boom may not see their time charters rolled over. The number of midsize units tied up at repair yards is also expected to shrink.

And while liner companies’ need to focus on costs is certainly less urgent than we anticipated earlier in the year, we expect liner company chartering departments will certainly not be relieved of pressure to minimise expenditure. Upside risk to our forecast here is certainly present, however.

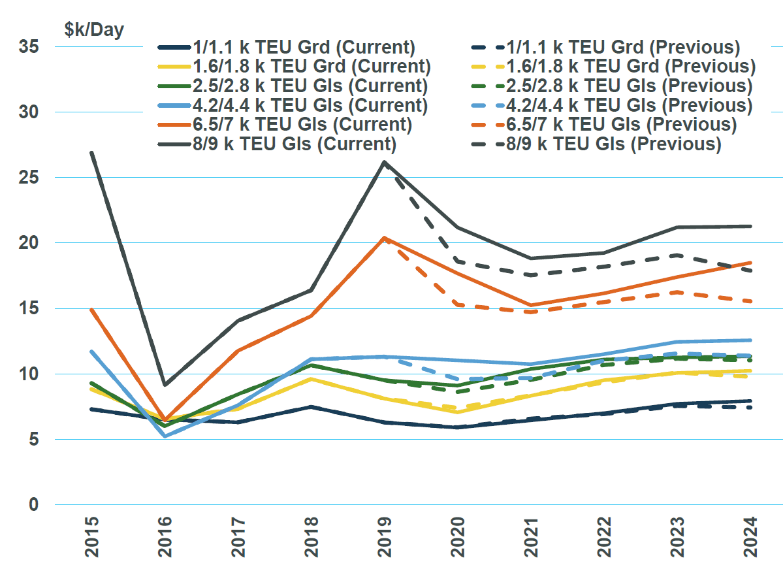

Revisions to our longer-term outlook have been fairly minor with this update, although as the chart above reveals we have adopted a more positive medium-term outlook for midsize units relative to recent updates. This reflects a mix of model recalibration, but also greater confidence that assets of this size will be able achieve earnings levels that are more consistent with what slot cost economics suggest they should. While we have arrived at this conclusion cautiously – aware that IMO 2020 and events this year have generated a large number of idiosyncratic shocks that have proven favourable to this size bracket – it is possible that 2017-18 was more of a transition period in terms of earnings than an equilibrium.

With that said, newbuild deliveries in the 10,000-15,000 teu size band will continue at a brisk pace in the next several years, and over time we anticipate market liquidity will increase. The past five years have been volatile ones for midsize vessels, and further surprises are likely in the years ahead.

This is guest post by Daniel Richards, senior analyst at Maritime Strategies International

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article