Cautious air cargo shippers delay tenders amid signs rates may have peaked

Air cargo shippers are increasingly delaying tender decisions and extending existing contracts, rather than locking ...

PLD: 'OPPORTUNISTIC DEAL-MAKING'PLD: REJECTED BY SEGROPLD: HUNTINGKNIN: BOND FINANCINGWTC: UP WE GODHL: NEW CFO APPOINTMENTFDX: TRADING UPDATE ON THE WAY TSLA: ON THE MENDGM: TECH STARTUP LISTINGDSV: NEW HIGH TARGET CHRW: BOLT-ON DEAL TIMEDHL: GO GREENDSV: BULLISH DSV: NOTE TO INVESTORSKO: TAX FIGHT

PLD: 'OPPORTUNISTIC DEAL-MAKING'PLD: REJECTED BY SEGROPLD: HUNTINGKNIN: BOND FINANCINGWTC: UP WE GODHL: NEW CFO APPOINTMENTFDX: TRADING UPDATE ON THE WAY TSLA: ON THE MENDGM: TECH STARTUP LISTINGDSV: NEW HIGH TARGET CHRW: BOLT-ON DEAL TIMEDHL: GO GREENDSV: BULLISH DSV: NOTE TO INVESTORSKO: TAX FIGHT

This article is compiled from IATA’s monthly international air cargo analyses, January to June

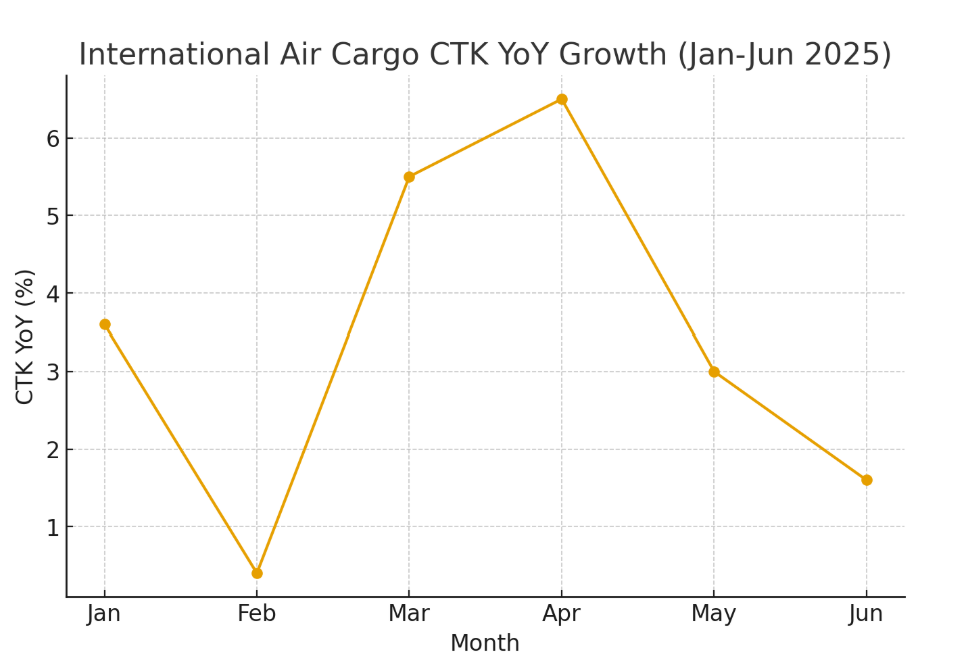

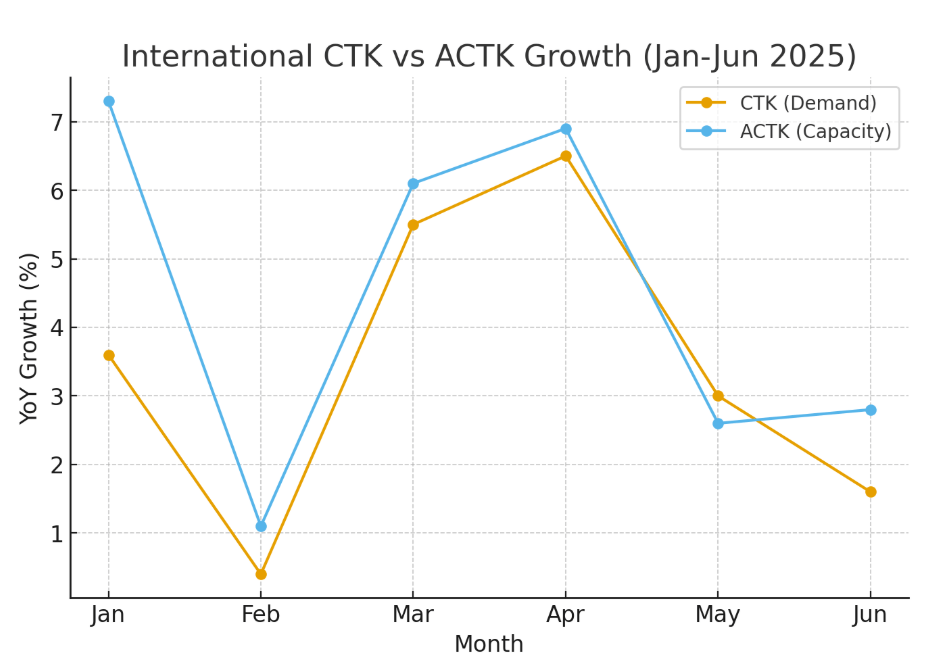

Global international air cargo demand expanded by 3.4% year on year in the first half of 2025, according to IATA’s monthly market analyses. Capacity, measured in available cargo tonne-km (ACTK), rose even faster, up 4.5% compared with the same period in 2024. This imbalance between supply and demand kept pressure on cargo load factors, even as demand remained in positive territory.

Demand outpaces, but growth moderates

The headline numbers underscore a market that is still expanding, but at a slowing pace. International cargo tonne-km (CTK) grew every month between January and June, though momentum weakened in the later months. The strongest demand increase came in April (+6.5%), boosted by tariff-driven front-loading and seasonal consumer flows. By June, growth had cooled to +1.6%, reflecting trade disruptions and a less supportive macroeconomic environment.

Capacity consistently outstripped demand in the early months. In January, international ACTK rose 7.3% against demand growth of 3.6%, while in April, ACTK growth of 6.9% slightly outpaced CTKs. Only in May did demand outpace capacity, with CTK up 3.0% versus ACTK at +2.6%.

Month-by-month:

Regional dynamics:

Outlook

With first-half international CTK up 3.4% and capacity up 4.5%, the air cargo industry has maintained growth despite a challenging trade backdrop. However, the slowdown in May and June points to a more uncertain second half. Geopolitical risks, tariff policies, and shifting shipping routes will continue to shape demand patterns.

Airlines now face the twin challenge of sustaining growth while navigating capacity deployment carefully to support yields. The first half of 2025 confirms that while air cargo remains resilient, competitive pressures will intensify.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article

Shafik Islam

September 14, 2025 at 1:50 pmI would like to know Cargo Export and import data from to Bangladesh and China. commodity and airlines wise .