Fifteen years of Cargolux results reveal air cargo’s uneven new era

Here at The Loadstar, we’ve been watching Cargolux for well over a decade. It has had its ups and downs – from financial stress ...

MFT: TAKING PROFIT DSV: LAYOFFS IN THE USATSLA: ON THE MENDCHRW: 'SPECIAL AWARD' TIMECHRW: NEW HIGH-END TARGET ON THE STREETDHL: ABOUT JET FUEL SUPPLYFDX: DISAPPOINTING DEBUT FOR LTL UNITWTC: MOMENTUMDHL: FLYING HIGHWTC: REBOUND ON WEAKNESS

MFT: TAKING PROFIT DSV: LAYOFFS IN THE USATSLA: ON THE MENDCHRW: 'SPECIAL AWARD' TIMECHRW: NEW HIGH-END TARGET ON THE STREETDHL: ABOUT JET FUEL SUPPLYFDX: DISAPPOINTING DEBUT FOR LTL UNITWTC: MOMENTUMDHL: FLYING HIGHWTC: REBOUND ON WEAKNESS

“Surprisingly, summer has been okay, volume-wise,” said one European airfreight forwarder this week.

“For us, June and July were the two strongest months in 2025, surprisingly. June is often good because it’s the end of the quarter. But July was still good. So, from that perspective, volume-wise, we’re not significantly going down; we’re maybe even slightly going up.”

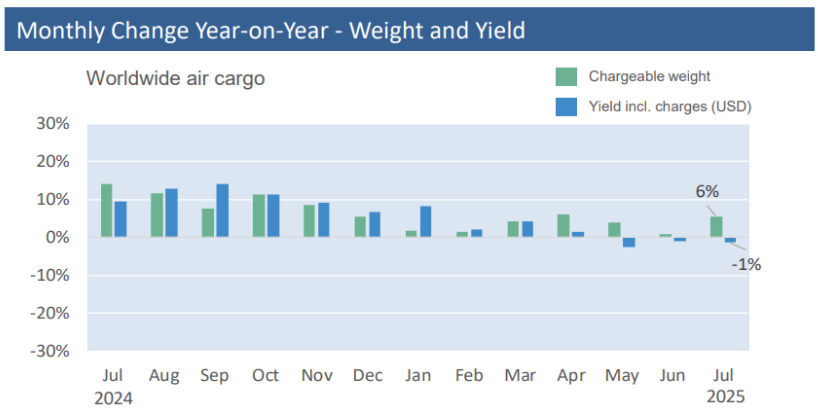

Despite much doom and gloom in airfreight, tonnages are not as poor as expected, and even saw a summer bump. WorldACD said this week that volumes out of Asia Pacific jumped 8% week on week, which it partially attributed to Japan’s return after a holiday.

“In a pattern similar to the corresponding week last year, global air cargo volume rebounded week on week (WoW) after three consecutive weeks of shrinking tonnage. Following declines of 1% in weeks 31 and 32 and a 6% slump in week 33, global chargeable weight increased 4% in week 34 (18-24 August).”

In fact, according to Rotate, August saw a 2% rise in freighter capacity over the average of the previous four months, although it was 1% down on July.

August’s biggest freighter capacity growth over the previous four months was focused on the transpacific, where westbound capacity rose 4%, and eastbound was up 5%. Latin America to North America was also up 5%, with capacity on those routes also higher than in July.

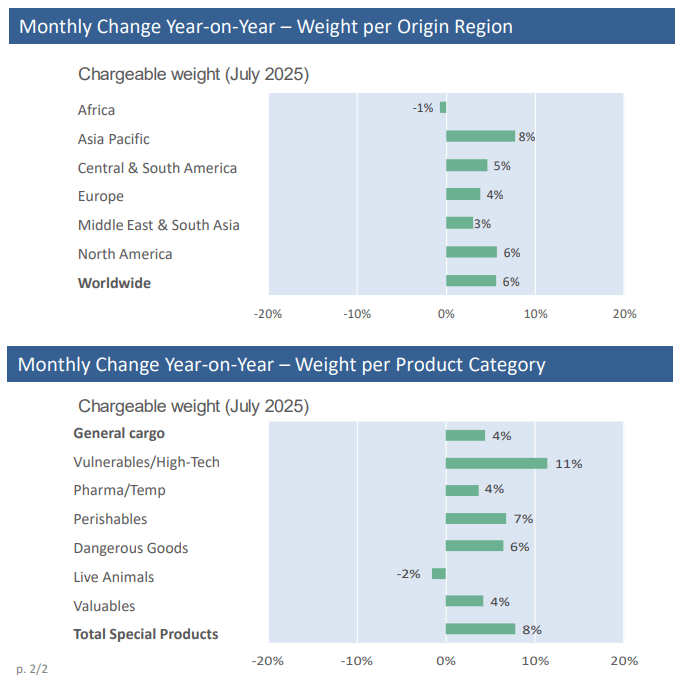

WorldACD noted that chargeable weight rose 6% in July over June, led by Asia Pacific-origin cargo, which went up 8% month on month. By category, general cargo was up 4%, while vulnerable and hi-tech cargo went up 11%.

Source: WorldACD

Although IATA has revised its volume forecast for 2025 downward, it still predicts 0.6% growth on 2024, to 69m tonnes – but below its initial projection of 72.5m.

“From a volume-wise perspective, it’s positive,” said the forwarder. “I think people are negative but I think it’s more the hesitance, the uncertainty, but it doesn’t seem that bad. I think the market is still growing.”

But while volumes don’t seem to be weak, margins are more of a headache. IATA forecasts cargo revenues to decline by 4.7%, to $142bn, while cargo yields are expected to fall 5.2%, “reflecting a combination of slower demand growth and lower oil prices”, it said.

The forwarder agreed that margins are under pressure.

WorldACD said that while average global rates went up 1% in week 34, over the previous week, with origin MESA up 4%, rates out of Europe were flat, and fell 1% from Asia Pacific, “impacted by a strong rebound of lower-yielding intra-Asia Pacific traffic”. It also showed weak yields since the start of the year.

Source: WorldACD

TAC Index noted yesterday that its overall rate index had risen 2.6% in the week to 1 September.

“Rates out of China rose, WoW, both to Europe and to the US, as well as … to Mexico. The new BAI spot rates from Hong Kong also maintained a firm tone over the week; and the overall index of outbound routes from Hong Kong edged slightly higher, by 1.4% WoW, to cut its decline to only 8.1% YoY. The outbound index from Shanghai gained 3.6% WoW.”

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article