The combined orderbook of non-operating shipowners (NOOs) has trebled over the past year, as they finally returned to the newbuilding market after a prolonged multi-year fire sale of their fleets to carriers.

According to this week’s Alphaliner report, NOOs had a combined 1.8m teu of capacity on order with shipyards at the end of March, compared with just 600,000 teu at the same point last year. That is in the 700 to 9,000 teu vessel sizes that typically comprise the “liquid” charter market, compared to the long-term charter market dominated by Seaspan.

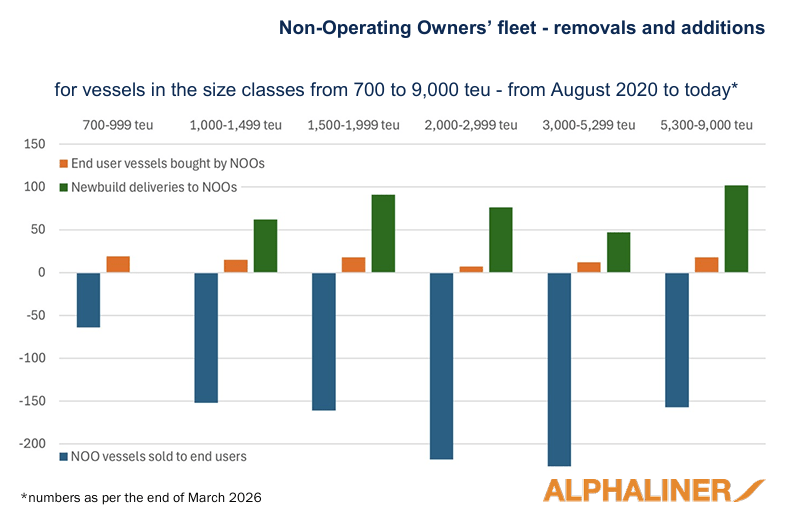

The declining number of ships under NOO ownership since 2020 has been one of the chief reasons that daily hire rates have remained so elevated, despite mostly weak spot freight rates.

Alphaliner said the combined NOO fleet was today 2.3m teu smaller than in late 2020, “when carriers started raiding the second-hand containership market in the Covid pandemic”.

The majority of that fleet ownerships transfer involved MSC, which has bought 415 ships, accounting for 1.6m teu of capacity, from NOOs since August 2020.

In the past 12 months, “MSC was again, and by far, the biggest buyer of NOO tonnage, with 65 ships for 230,000 teu joining its fleet, of which only 17 units were already on charter to the Switzerland-based company”, the analyst noted.

However, in the past year, NOOs signed a series of newbuilding contracts that show a renewed appetite for modern tonnage.

“The year 2025, and particularly the second half, saw a welcome rally in newbuilding orders from NOOs that has extended into the first quarter of 2026,” Alphaliner said.

Once again, certain vessel sizes dominated the orderbook: the 5,300 to 9,000 teu class saw 90 orders placed, for a combined total of 630,000 teu; the 3,000 to 5,300 teu class saw 116 ships ordered, for 435,000 teu; while intra-Asia favourite, the 1,500 to 1,900 teu Bangkok-max class saw 71 vessels ordered, for 130,000 teu.

Source: Alphaliner

However, Alphaliner added that the new ships being built for NOOs were unlikely to alleviate the short-term capacity issues and cost elevation of the current liquid charter market.

“The replenishment of the NOO fleet is a positive development for the charter market, but will only partly fix the market’s short-term problem for carriers, which is its increasing lack of liquidity, especially in some sizes.

“The majority of vessels ordered by NOOs are covered by long-term charter employments, including in some cases smaller units of the ‘Bangkok-max’ type of 1,800 teu.

“As a result, many of these new ships will not be traded in the charter market for several years to come, and will thus not be able to meet ‘day to day’ requirements from carriers,” it said.

Comment on this article