Why I’ll miss the ‘defiantly brazen’ Schenker

The picture heading this article forever memorialises a sad day for Panalpina’s long-term staff, customers ...

FDX: ABOUT USPS PRIVATISATIONFDX: CCO VIEWFDX: LOWER GUIDANCE FDX: DISRUPTING AIR FREIGHTFDX: FOCUS ON KEY VERTICALFDX: LTL OUTLOOKGXO: NEW LOW LINE: NEW LOW FDX: INDUSTRIAL WOESFDX: HEALTH CHECKFDX: TRADING UPDATEWMT: GREEN WOESFDX: FREIGHT BREAK-UPFDX: WAITING FOR THE SPINHON: BREAK-UP ALLUREDSV: BREACHING SUPPORTVW: BOLT-ON DEALAMZN: TOP PICK

FDX: ABOUT USPS PRIVATISATIONFDX: CCO VIEWFDX: LOWER GUIDANCE FDX: DISRUPTING AIR FREIGHTFDX: FOCUS ON KEY VERTICALFDX: LTL OUTLOOKGXO: NEW LOW LINE: NEW LOW FDX: INDUSTRIAL WOESFDX: HEALTH CHECKFDX: TRADING UPDATEWMT: GREEN WOESFDX: FREIGHT BREAK-UPFDX: WAITING FOR THE SPINHON: BREAK-UP ALLUREDSV: BREACHING SUPPORTVW: BOLT-ON DEALAMZN: TOP PICK

Panalpina chief executive Peter Ulber was unequivocal on targets for the Swiss freight forwarder this year: “To focus on opportunities that will drive growth organically, by way of acquisitions and through innovation, and to continue to improve productivity and optimise costs across all businesses and geographies.”

So, what’s next for Panalpina as sea and air freight volumes are unlikely to surprise on the upside into 2017, and its shares look fully priced?

Options

Options appear thin on the ground, even for a company of Panalpina’s size, which ranks among the major air and sea freight forwarders globally. I wonder whether its management team is ambitious enough to engineer a deal of the size that would transform its cyclical portfolio of clients into a more defensive and diverse collection of corporate accounts.

Aside from certain freight forwarding activities within CEVA, there are not many takeover candidates available and, in any case, Swiss companies tend to be very conservative when it comes to acquisitions. In this context, it is easier to speculate that Panalpina could itself be taken over by a player such as CH Robinson, which needs scale in sea freight, although it may be interested in other supply chain assets.

So, any swift change in its corporate strategy, which focuses on organic growth, is unlikely. But as cyclical swings persist, shareholder value is at stake, and there appears to be little residual value in Panalpina stock, apart from an appealing forward yield hovering around 3% – which has doubled in less than three years, mainly due to a falling share price.

Assuming a weighted average cost of capital of between 8% and 10%, top-line growth in line with inflation into 2019, an ebitda margin rising 100 basis points over the period and a 14x adjusted cash flow multiple, the net present value of Panalpina’s enterprise ranges between Sfr2.7bn (US$2.8bn) and Sfr2.8bn, meaning that its shares are almost fully valued currently at Sfr120.7 each.

It is worth considering that, barring dividend payments, Panalpina has not delivered any value in terms of capital appreciation over the past decade, and its trailing five-year performance was similarly disappointing.

Headwinds

While it appears to be serious about entertaining shareholder-friendly activity, I still need to be convinced that it is ready to crack on with a more aggressive corporate plan.

Recent activity was limited to the acquisition of a majority stake in Kenya’s Airflo. This was a bolt-on deal; the amount was undisclosed but it is surely just a drop in the ocean in terms of size for a Sfr2.8bn market-cap company operating in a very challenging industry, which last year “was marked with consolidation (…) by both competition and carriers, while new competitors continued to enter the market”.

A crowded, possibly stagnating freight forwarding market means a smaller profit pool, resulting in more pressure on margins, although scale has helped Panalpina and the majors preserve their underlying profitability. Macroeconomic headwinds, however, come on the back of meaningful currency volatility, which continued to weigh on profits and badly impacted its performance in recent quarters.

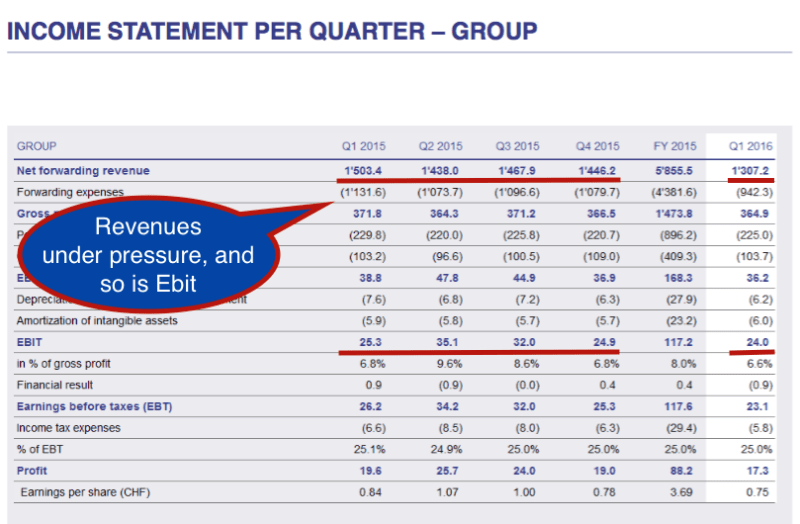

Its first-quarter results released on 21 April show the extent of the problem.

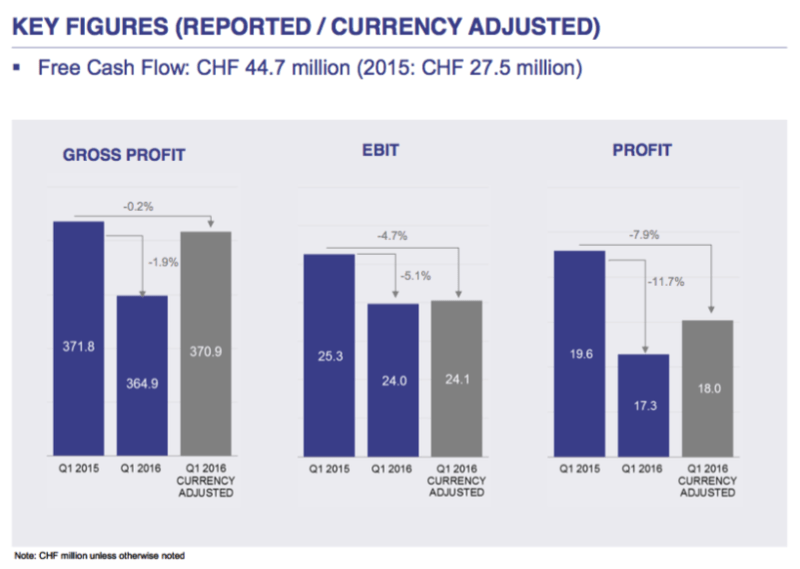

Source: Panalpina

Financial efficiency

Panalpina was quick to point out in its latest investor presentation that quarterly free cash flow in the quarter ending 31 March was Sfr44m, up 62% year-on-year, but that surge was mainly due to an 11% drop in receivables rather than growing core cash flows, which were essentially flat year-on-year at Sfr36.6m.

Meanwhile, its rising gross cash pile was up 26% to Sfr435m year-on-year, but that also represents its net cash position, given a debt-free balance sheet.

Near-zero interest rates and low spreads over Libor should be an incentive to take on debt, particularly because the group is facing a prolonged downturn in the oil and gas sectors, where many of its clients operate.

As most of the work that Panalpina performs with engineering companies comes traditionally from the oil and gas industry, the impact of these developments on its energy solutions unit was “considerable”, it said in its annual results, adding that it was taking the necessary steps to diversify from more cyclical industries.

Plunging commodity prices impacted the energy industry so badly in 2015 that “neither Panalpina nor its customers were spared the effects”, with the end result of fewer investments being approved and projects being either postponed indefinitely or cancelled.

Panalpina noted that “the extremely soft market in both ocean freight and air freight, combined with increased rate volatility, led to intensified speculation in the market and further exacerbated the situation”. First-quarter results painted a similar picture.

Good news?

The good news, however, is that Panalpina might know already where to invest its dollars.

A bright spot last year was the performance of “consumer and retail, and fashion verticals, ocean freight operations, with strong growth in the Far East westbound trade”. It also recorded decent growth in both volumes and gross profits across global and SME accounts by implementing combined order- and freight-management solutions with key customers.

“In parallel, the company focused on tailored consolidation of buyers to optimise cargo flow for customers,” it added.

And despite the fact that at operating level, it recorded its worst performance since the first quarter of 2015, it seems that some of its key financial metrics bottomed out in the first quarter of this year.

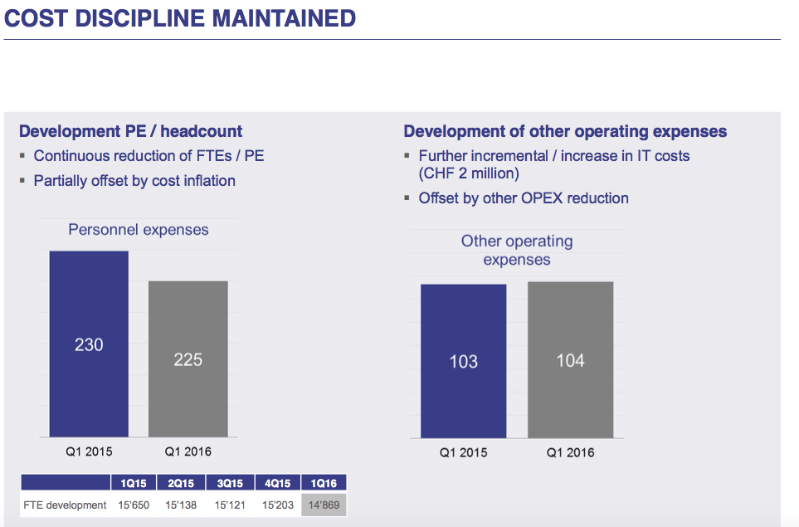

Source: Panalpina

Margins are holding up, and Panalpina is changing as well as protecting its client portfolio, but changes will take time.

As it brags about its “biggest success” – which involved “global order and freight management for major companies in the consumer market, where Panalpina is moving from a third-party logistics provider to a lead logistics provider role” – the recent spotlight is on other news, indicating that it is rationalising its geographical footprint.

Source: Panalpina

Our sources say Panalpina is closing its facility at JFK Airport and moving its operations to Chicago, with 35 jobs being lost in New York. That is a small number, of course, but if cyclical headwinds do not fade, additional lay-offs should not come as a big surprise to our readers.

Comment on this article