Hormuz 'definitely shut', landbridges under pressure – TIR to the rescue?

With tentative hopes of a reopening of the Hormuz Strait dashed by the wave of ...

WTC: ANOTHER DIFFICULT WEEK CHRW: NEW PRODUCT LAUNCHDSV: LEADING THE DROP RXO: CRATERINGDSV: WHAT TO LIKEDSV: BULLISH BAMZN: 'AI EDGE'HD: HERE IS HOW IT LOOKSAMZN: REG RISKMAERSK: MOST HARMED

WTC: ANOTHER DIFFICULT WEEK CHRW: NEW PRODUCT LAUNCHDSV: LEADING THE DROP RXO: CRATERINGDSV: WHAT TO LIKEDSV: BULLISH BAMZN: 'AI EDGE'HD: HERE IS HOW IT LOOKSAMZN: REG RISKMAERSK: MOST HARMED

Shippers are paying significantly less for container transport, in real terms, than they were more than a decade ago, according to new analysis from Sea-Intelligence, based on Container Trade Statistics (CTS) data.

The consultancy found that, once inflation is accounted for, global average freight rates are now between 40% and 65% lower than in 2008/2009, underlining the long-term erosion in real pricing power for carriers, despite periodic rate spikes.

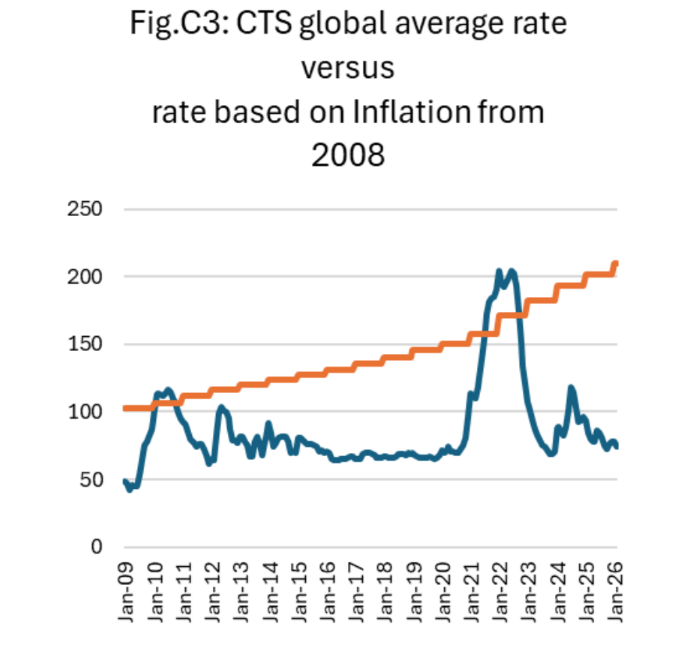

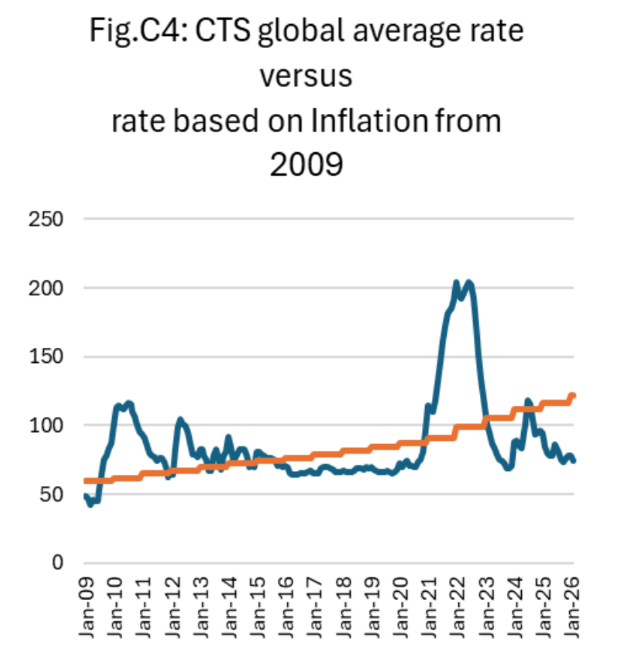

The CTS Pricing Index measures rates at the time of cargo loading and uses 2008 as a baseline. The index dropped sharply in 2009 due to the financial crisis, but since then, the trajectory of rates has diverged significantly from inflation.

Comparing actual rates with an inflation-adjusted benchmark, Sea-Intelligence found that, “for the vast majority of the time, the actual freight rates have been substantially below the inflation adjusted line”.

Source: Sea-Intelligence

The only notable exceptions were short-lived periods of disruption, including the post-financial crisis capacity crunch in 2010 and the peak of the pandemic-driven supply chain crisis.

Even the Red Sea disruption in early 2024 resulted in only a modest rise, relative to inflation-adjusted levels when using a 2009 baseline.

Source: Sea-Intelligence

Sea-Intelligence noted that the choice of baseline year materially affected the analysis, given the stark difference between rate levels in 2008 and the crisis-hit 2009 market. Nevertheless, both approaches point to the same conclusion: real freight rates have consistently lagged inflation.

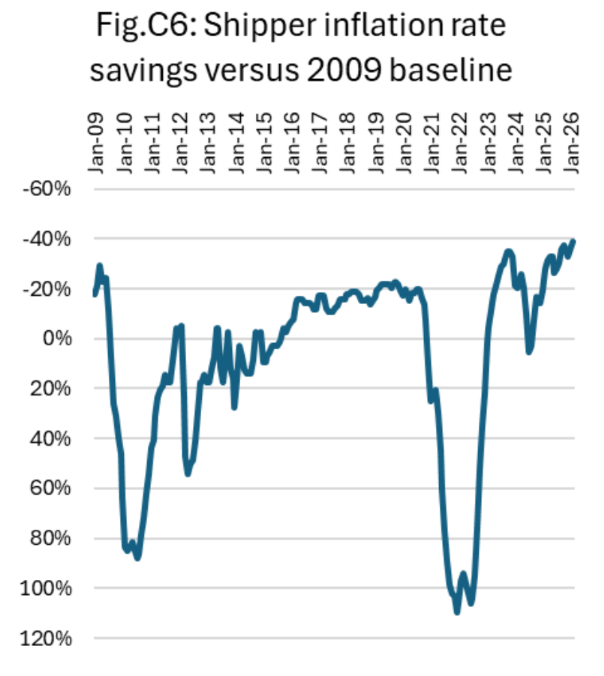

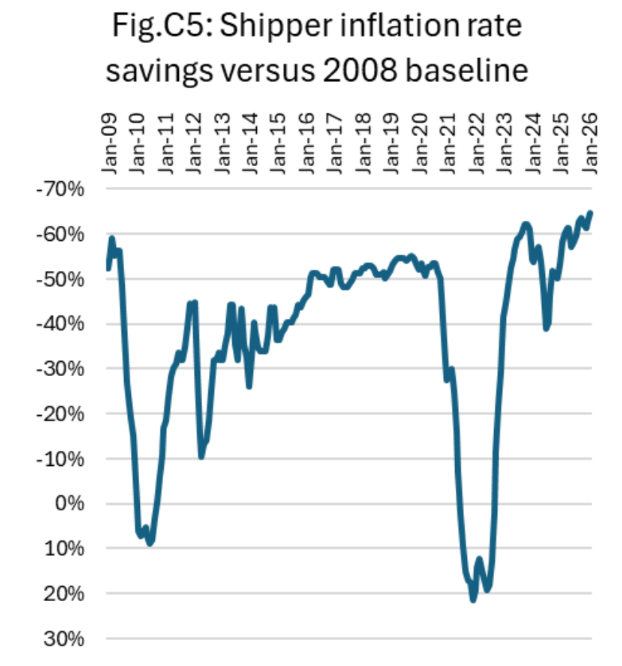

Figures comparing the gap between actual and inflation-adjusted rates show the index frequently negative relative to the baseline, indicating that real rates are below historical levels.

Source: Sea-Intelligence

Sea-Intelligence explained: “Whenever this is the case, it means global average freight rates, in real terms, are lower than in 2008 or 2009.”

The latest CTS data, for February 2026, underscores the scale of the decline.

“The global rate level we see now is at a point where, in real terms, rates are 40% lower than where the rates were in 2009, and 65% lower than where they were in 2008.”

For shippers, this represents a substantial cost saving long term, even as short-term volatility continues to characterise container freight markets. This short-term volatility is currently being seen amid the Middle East disruption, and closure of the Strait of Hormuz and subsequent vessel re-routings, which will be reflected in CTS’s March and April price-index reports.

As highlighted by The Loadstar’s managing editor, Gavin van Marle, on The Loadstar’s recent News in Brief Podcast: “Spot rates, as in just the rate for the freight, are actually still in a weak place. But freight costs, thanks to the war, are on the rise.”

“These increases are largely driven by the implementation of new fuel surcharges,” Mr van Marle explained, and highlighted the 30-day lag between carrier’s ability to announced surcharges before implementing them.

Watch our latest News in Brief Podcast on YouTube and subscribe so you never miss an update!

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article