Forwarders fear for time-critical cargo as Kenya plans new security measures

Kenya’s proposed Strategic Goods Control Bill has opened a new debate over whether tighter security ...

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

All eyes in the logistics industry are on Ceva and Hyundai Merchant Marine nowadays, but a potentially bigger story captured the attention of supply chain managers last week when DHL Global Forwarding (DGF) appointed Tim Scharwath (pictured) as its new chief executive.

Deutsche Post DHL said on 18 May that during his tenure at Kuehne + Nagel, Mr Scharwath had been “accountable for the migration of different country organisations, the integration of acquired companies and the successful management of his business during the economic downturn in 2009”.

A K+N board member since 2011, Mr Scharwath also held a position as account manager spanning the retail and hi-tech industries during the 1990s. His track record fits perfectly, given the challenges posed by the changing dynamics that characterise those industries, key to DGF’s value proposition with clients.

Mr Scharwath will start within the next 12 months, but undoubtedly his appointment already gives DGF’s strategy a completely different taste.

And – regardless of a soft market and the company’s past troubles, most of them IT-related – DGF clearly remains in a strong position to expand its global reach at a time when a few other players are pulling all the stops to grow inorganically in the freight forwarding market.

Predator

DGF was the subject of much speculation earlier this year when it was rumoured to be a takeover target for Japan Post. With the appointment of Mr Scharwath, I suspect DGF could turn from prey to predator sooner rather than later, turning its attention to the public markets by 2020.

On the face of it, Mr Scharwath’s reputation adds credibility to DGF’s turnaround plan after one of the worst years on record, particularly when it comes to possible cross-border deals, the smooth integration of already acquired assets and extraordinary corporate activity.

As we expected a year ago or so, DP-DHL shares continue to trade at paltry multiples, and a partial spin-off of DGF would likely release value, not only for DGF holders, but also for the shareholders of the parent company, according to my preliminary calculations.

Before that happens, of course, Mr Scharwath must solve a challenging technology puzzle, hoping that DGF’s IT environment will soon be up to speed in what remains a very challenging market for freight and forwarding activities.

Roadmap

DP-DHL said in its first-quarter results that DGF’s “turnaround agenda and IT renewal roadmap [are] making good progress” as it continues to invest in turnaround measures as well as in warehouses and office buildings, technical equipment and machinery. However, its financials indicate that this turnaround story might need a little boost from M&A to thrive, or at least to cope with challenging trading conditions.

Given that DP-DHL doesn’t seem to want to shrink its asset portfolio – which remains the most obvious value-accretive option, in my view – then it could consider acquisitions; looking for cost and revenue synergies across the DGF unit, which is much lighter in terms of staff requirements than the reminder of its portfolio.

As you may know, the German government owns a large stake in DP-DHL, but it should acknowledge that shareholder value is still at risk after a year during which the dividend was unchanged and significant paper losses were recorded.

It’s not even that rapidly rising income streams are on the cards – DP-DHL’s guidance for underlying income indicates that a 5-10% rise in dividends per share from €0.85 is possible this year, but there are operational risks associated with those estimates, while investor trust remains a serious issue for the board.

Its stock currently languishes at €26, having trailed the DAX Index by 14 percentage points in 2015. It is down only 11% over the past 12 months against a 17% drop for the benchmark index, although the DAX was pushed down almost 10% by the Volkswagen emissions scandal in mid-September.

Numbers

In the first quarter, DGF (23% of group sales) was the fourth revenue contributor at group level, with a top-line of €3.15bn, excluding internal revenues of €175m. It ranked behind PeP (Post, e-commerce and Parcel) which constituted 30% of sales, turning over almost €4.2bn, and Supply Chain (24%), but was slightly above Express (23%) once internal revenues are taken into account.

The numbers become more interesting, and explain why the turnaround of DGF is so important, once you consider the total number of employees per unit and the amount of unit revenue divided by staff – the revenue-employee ratio, on a quarterly basis, stands at €24,800 for Pep, €23,200 for Supply Chain and €38,200 for Express.

Given its lowly investment requirements, DGF is the star performer based on this metric, boasting a revenue-employee ratio of €73,000. DGF becomes less attractive, however, when it comes to the EBIT-employee ratio, recording a lowly €1,180 (due to its low level of profitability), which compares with €2,450 for PeP, €4,322 for Express and €875 for the supply chain unit.

DGF still has some problems and is not as healthy – dare I say it – as some tobacco industry players, but all these elements indicate that DGF probably deserves more attention with regard to growth alternatives than any other assets in DP-DHL’s diverse portfolio; and if it returned closer to its trailing normalised level of profitability, it could surely attract interest from institutional investors as a standalone entity over the medium term.

Pressure

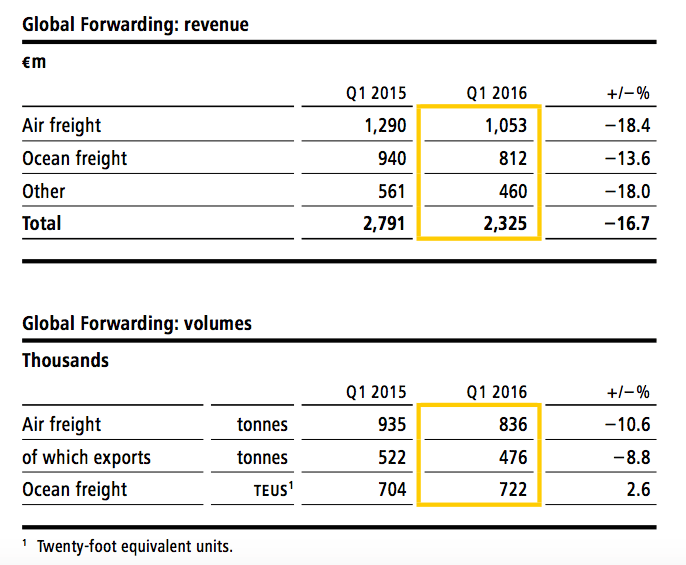

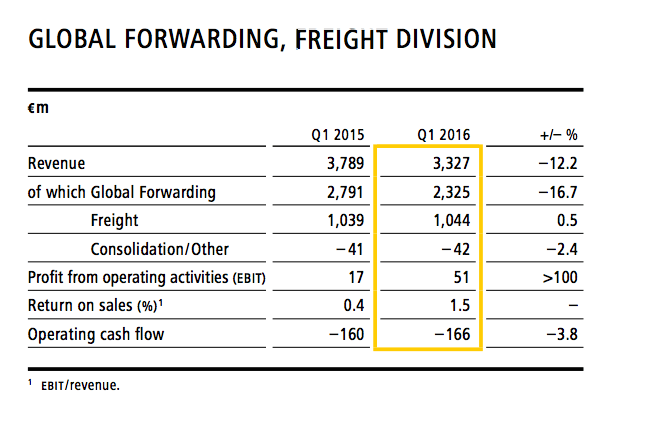

Delving into the details of its first-quarter results, revenues in air and ocean freight fell 12.2% year-on-year, but EBIT improved and return on sales was on the up, although its performance is by no means encouraging, as the tables below show.

Source: DP-DHL

Source: DP-DHL

The group said that “compared with the previous year, air freight volumes declined, whilst ocean freight volumes increased slightly”.

It added that air freight volumes fell by 10.6% as a result of a declining market and “measures we implemented in the previous year, which included withdrawing from selected business activities with insufficient margins”.

It said: “We have, however, secured additional new business during the reporting period, which will be implemented as the year progresses and is expected to have a positive impact on volume development.

“Air freight prices remain under pressure due to large surplus capacities and low fuel costs, which reduced our revenue by 18.4% and gross profit by 4.5% in the first quarter of 2016. Ocean freight volumes were up by 2.6% in the reporting period, with exports from Asia and the intra-Asia volumes driving most of the growth.”

This article is © The Loadstar. Reproduction, rewriting, or derivative use requires a license. Contact [email protected] for licensing enquiries.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article