Why Hapag-Lloyd's Eurogate Hamburg stake matters & what's next

Could Eurokai also be a target for Hapag?

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

VW: THE LAST CUT IS THE DEEPESTJBHT: GEARING UP VW: BUYING TIMER: BIG VOTE OF CONFIDENCEAAPL: BEARISH HEDGEYE AAPL: THE BEAR CASEFDX: LIFE SCIENCES ORG UNVEILEDWTC: UPS AND DOWNSWTC: ASX ANNOUNCEMENT REGARDING DSV PARTNERSHIP VW: D-DAYPLD: KEEP PUSHINGDHL: NEW AIR SERVICEDHL: GUIDANCE UPGRADE REACTION

“Kerry Logistics is becoming the major logistics provider for the Silk Road of the 21st century, both overland and maritime,” according to George Yeo, president of Kerry Logistics Network, announcing 2015 annual results.

What a difference two years can make.

Expectations were high in December 2013, when Hong Kong-based 3PL Kerry Logistics launched its IPO. Less than a month later, its shares had already appreciated by 40% on the domestic stock market, changing hands at over HK$14.

“All the IPOs are up, it doesn’t matter whether it’s a donkey or a dog,” a local broker told Bloomberg after a slew of public offerings, ironically or not led by a Chinese graveyard developer, came to the Hong Kong market.

Since, however, Kerry shareholders have had to digest trading updates that have done little to boost the value of their holdings, and the recently announced annual results were no exception.

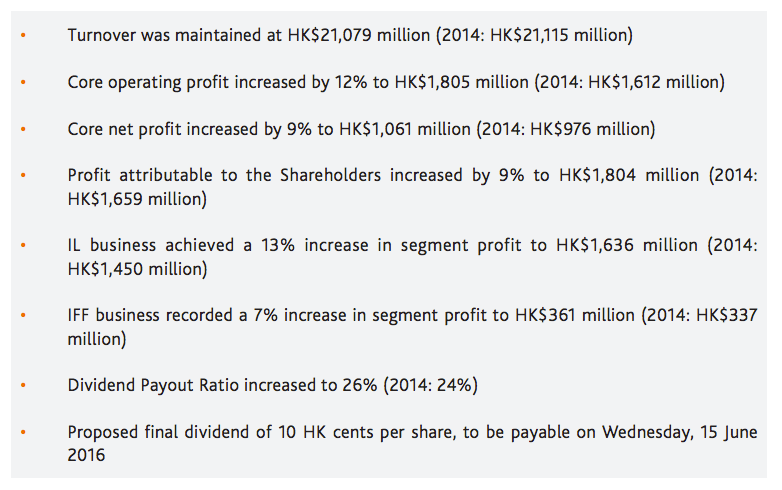

The table below shows some key financial highlights.

Unadjusted revenues, which include benefits from acquisitions, were flat at HK$21bn, while core margins rose on the back of lower freight and transportation costs that more than offset higher administrative expenses at group level, yielding a high single-digit growth in earnings per share (EPS).

A surge in EPS is surely encouraging – after all, its share count was virtually unchanged on an annual basis, so greater earnings power clearly came from careful management of direct costs in a challenging environment for the forwarding and logistics industry.

“In 2015, Kerry Logistics forged ahead with resilience against headwinds,” it said in its annual results.

“The macroeconomic volatilities, instabilities in Europe, currency fluctuations across Asian nations, and China’s slowing GDP growth exerted pressure at an increased magnitude.”

Valuation

Despite significant challenges, it’s remarkable that Kerry still managed to grow core earnings for the seventh year in a row.

Still, its enterprise value is just about eight times its forward adjusted operating cash flow, while its market value, which excludes net debt, is 14 times forward net earnings – these are lowly trading multiples when compared with those of more mature 3PL businesses such as DSV, Kuehne & Nagel, CH Robinson and Expeditors.

While Kerry is bullish about growth prospects and the resilience of its business model, its current valuation also implies a significant discount to those of both bigger and smaller rivals from outside Asia, spanning XPO Logistics and Echo Global Logistics as well as Radiant Logistics.

Why so?

Lofty trading multiples and an equity premium can be achieved if Kerry manages to grow sales and margins at a faster pace while also delivering rapidly rising dividends – its forward yield is 1.5% versus 0.8% in 2013 at constant share prices.

That combination of factors is arguably needed to keep its shares well above the IPO price of HK$10.20 – the high end of the float range. To achieve greater returns spurred by cost savings, Kerry must expand its asset base by growing inorganically, just as it did in 2015, but it’s a delicate balancing act as such a corporate action would also mean higher risks for investors.

Its next acquisition appears to be around the corner, as it revealed that has an agreement to buy a US-based ocean freight forwarder. The name of the target has so far remained undisclosed, as are any financial details.

Regardless of its future corporate strategy, its market listing so far has proved to be a great marketing story, sold to investors at the right time, as well as a textbook example of a firm whose equity was massively overvalued when Kerry Properties Ltd (KPL) – its parent company and the controlling shareholder post-IPO – managed to spin it off successfully.

As a pure-growth play focused on Asia, the argument went at the time of its IPO, Kerry would likely continue to attract cheap capital to fund new investment and stellar growth prospects. As it turned out, everybody in the industry now faces deflationary forces in the trade, which render debt payments heavier – while signs of political and economic instability in the Middle East and South-east Asia also do not bode well with growth.

Moreover, one obvious issue is that KPL is unlikely to dilute its 42% stake any further in order to increase the free float and boost thin trading volumes, which currently indicate that less than one million shares have been traded daily since the turn of the year. KPL receives a hefty dividend – a steady income stream helps it reduce, at least partly, the volatility of its own business, which has struggled to meet bullish expectations in the last 12 months.

Price and diversification

The share price action in recent weeks says it all, really. Now trading at about HK$11, some 23% below its record high of January 2014, the stock has had a challenging year so far: it hit a record closing low of HK$9.68 in mid-January, when stock market investors worldwide were spooked by surging volatility across industries.

With the direction of global monetary policies still uncertain, management is right to be cautious when it comes to capital deployment, given that organic growth is nowhere in sight and accretive buybacks, however they are financed, could simply be a waste of money. Additionally, its net leverage leaves it only limited room for action, in my view.

At the end of the year, Kerry said it managed a logistics facility portfolio of 45m sq ft, of which 24m sq ft were self-owned. It’s eager to grow from there, while recording rising returns outside its own turf, but its Asia-centric portfolio of assets exposes it to currency risk that ought to be managed by diversifying out of Asia – hence the purchase of the US-based forwarder.

As it did in past deals, Kerry is likely to snap up a majority stake in the acquired businesses, while maintaining a strong focus on assets that will give it a competitive advantage in the Chinese e-tail market.

“E-commerce will remain an important growth factor for Kerry Logistics in the coming years. Having launched the first cross-border e-commerce logistics service in Ningbo, mainland China, the group looks to expand into other cross-border trade pilot cities and zones,” it reiterated in its annual results.

Deals and investment

Size-wise, any takeover engineered by Kerry management will likely be inside the $150-$250m range, given its cash balances, cash flow generation, capital requirements and overall indebtedness.

Its push aimed at growing abroad means that deal-making in France, Italy and Turkey is also a distinct possibility, at least according to European managing director Thomas Blank, who was hired at the end of 2015 and has over 35 years of experience in logistics and freight forwarding. Mr Blank and his European team have a lot of work to do because Europe was the worst performing region in 2015.

Kerry could also use more leverage to push up return on equity – a key metric for a firm at this stage of maturity – while chasing growth wherever it wants to around the globe, but precious funds will also have to be devoted to its own business development plan.

In this context, additional investment in IT infrastructure is also of paramount importance.

Financial details are sketchy, but the group said it “opened its first IT development centre in Penang, Malaysia in January 2016 to harness internet technology in support of its rapidly growing international operation and rising demand for IT application system.

“As part of its overall IT development strategy, Kerry will leverage Penang’s established strength and use it as a base for an offshore IT support centre to share resources amongst different offices globally, in a bid to increase operational efficiency.” And, I’d add, to create value, if it truly aims to become a major operator for the Silk Road of the 21st century.

For uninterrupted access, sign in or sign up to The Daily News, Premium or The Loadstar Enterprise Plan.

Comment on this article